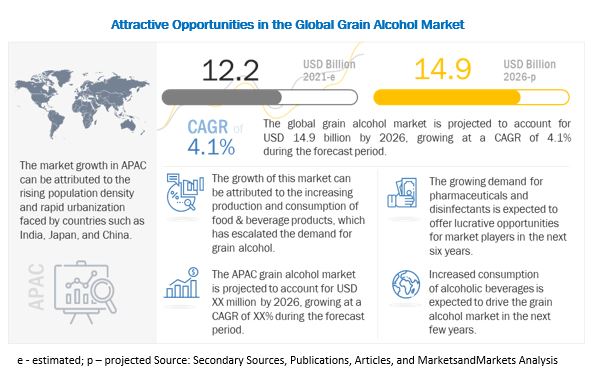

The report "Grain Alcohol Market by Type (Ethanol, Polyols), Application (Food, Beverages, Pharmaceutical & Healthcare), Source (Sugarcane, Grains, Fruits), Functionality (Preservative, Coloring/flavoring agent, Coatings), and by Region - Global Forecast to 2026" is estimated at USD 12.2 billion in 2021; it is projected to grow at a CAGR of 4.1% to reach USD 14.9 billion by 2026. The increase in demand for grain alcohol in various industries such as food & beverages and health & personal care is driving the grain alcohol market globally. The grain alcohol market is gaining momentum due to the increase in beer production and increasing demand for craft beer. The use of ethanol in the beverage industry has resulted in the growth in the market of grain alcohol for beverage applications. Grain alcohols are used as preservatives, food color, or coatings in the end products. The market for grain alcohol is largely associated with the sale of beverage products. Increasing sales of a variety of beverage and health & personal care products in matured markets of developed economies in the last five years are responsible for the increased growth of the grain alcohol industry.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=8581594

Ethanol sub-segment in by type segment is estimated to account for the

largest share in the grain alcohol market.

Ethanol is widely used in the food industry as a flavoring and coloring agent and in candy glazing. The antimicrobial property of ethanol helps it to be used in pharmaceuticals for medicinal applications. It is very commonly found in cough syrups. Ethanol is an excellent solvent; due to its solubility, ethanol finds its usage in manufacturing antibiotics, tablets & pills, vitamins, and in a variety of medicines.

In by source segment, the fruits sub-segment is projected to account

for the fastest market growth in the grain alcohol market.

Alcohol can be produced by fermenting a sugar-containing mash of fruits such as grapes, berries, and apples. Grapes are the most commonly used raw materials for alcohol fermentation to produce alcoholic beverages such as wine and brandy. Apples and citrus fruits, when added with sufficient fermentable sugars, are crushed and fermented. Their use in production of premium quality alcoholic beverages such as wines, is estimated to increase their usage in the market.

Beverage sub-segment by application is projected to account for the

largest market share of the grain alcohol market over the forecast period.

Alcoholic beverages are estimated to account for the largest market share in the global grain alcohol market, as globall populations in developed and developing economies show a rising trend for consumption of alcoholic beverages. The manufacturers are also investing into development of newer customized lproduc ts for attracting consumer interest and sales for their products. These are estimated to account for the strong growth of the segment.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=8581594

North America is estimated to dominate the global grain alcohol market

over the forecast period.

The rising consumption of and demand for alcohol has resulted in the use of grain alcohol for beverage applications. In North America, the US is one of the dominant grain alcohol markets. Beer, spirits, and wine are largely consumed alcoholic beverages in this country. The country has no specific law that forbids consumption of alcohol in public but enforces strict laws on age limit for its consumption and purchase. According to the Organisation for Economic Co-operation and Development (OECD), Canada has milder levels of taxation of alcohol at the federal level, but minimum prices and markups are enforced in several provinces, which contribute to raising prices. These trends account for the strong share of the region in global market.

The key players in this market include ADM (US, Cargill (US), Wilmar Group (Singapore), Merck Group (Germany), and Roquette Frères (France). These players in this market are focusing on increasing their presence through agreements and collaborations. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.