The report "Trace

Minerals In Feed Market by Type (Iron, Zinc, Manganese, Copper, Cobalt,

Chromium, Other Types), Livestock , Chelate Type (Amino Acids, Proteinates,

Polysaccharides, Other Chelate Types), Form, And Region – Global Forecast To

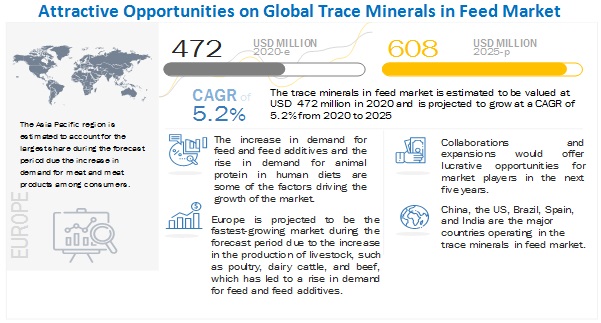

2025", The global trace minerals in feed market size is estimated to

be valued at USD 472 million in 2020 and is expected to reach a value of USD

608 million by 2025, growing at a CAGR of 5.2% during the forecast period.

Factors such as the rise in production of compound feed, and the increase in

the importance of protein-rich diets among consumers across the globe opened

new avenues for trace minerals in feed market. The major feed producing

countries in the world include China, the US, Brazil, Mexico, Spain, India, and

Russia. The where the demand for chicken and red meat has been growing. This in

these countries, which has also contributed to the growth of the market.

Download PDF Brochure

@ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=196308436

Iron, by type, is estimated to

hold the largest market share during the forecast period

The market for trace minerals in

feed, by type, has been segmented into iron, zinc, manganese, copper, cobalt,

chromium, other types which include selenium and iodine. iron is considered the

main constituent in the formation of hemoglobin and myoglobin, as it supports

the transport of oxygen to all parts of the body. The deficiency of iron causes

stunted growth, pale mucous membranes, anemia, and diarrhea in livestock. The

iron segment accounted for the largest share in the trace minerals in feed

market, as livestock species are most commonly affected by deficiencies of

iron, which causes oxidative stress and anemia. In the recent years, the EU has

approved iron compounds, such as ferric chloride hexahydrate, ferric oxide,

ferrous carbonate, ferrous chelate of amino acids, ferrous chelate of glycine

hydrate, ferrous fumarate, ferrous sulfate heptahydrate, and ferrous sulfate

monohydrate, without a time limit for use as a feed additive. Due to its higher

acceptance among regulatory bodies, the market for iron as a trace mineral in

feed is projected to witness a high growth rate during the forecast

period.

Poultry, by livestock, is estimated to hold the largest share in the

trace minerals in feed market during the forecast period

The poultry segment accounts for

the largest share and is also projected to grow at the fastest rate during the

forecast period. There has been a significant increase in demand for poultry

meat and other byproducts across the globe. People are therefore engaging in

animal rearing and animal husbandry to fulfil this global demand. The most effective way to achieve the highest

production is to supply these birds with trace minerals, such as zinc, copper,

and manganese, to increase their performance, which has led to an increase in

demand for trace minerals. Trace

minerals are indispensable components in poultry diets. They are required for

the growth, bone and feather development, and enzyme structure. The immune

functions of all poultry species depend on trace minerals. This drives the

growth of trace minerals in feed market across the globe.

Amino acids, by chelate type, is estimated to account for the largest

market share during the forecast period

Amino acids are considered an

ideal chelator due to their ability to be easily absorbed in the animal body.

This is due to the attachment of amino acids to the mineral molecules that

create a more stable structure, which helps the minerals survive in the acidic

environment of the stomach. Furthermore, trace minerals are protected from

various bacteria present in the body of animals, and enzymes are unable to

degrade it. It also inhibits the antagonistic action between metal ions and

decreases the breaking down of vitamins in the feed. This is due to their

ability to be easily absorbed in the body for the normal functioning of protein

synthesis. This increases the absorption of minerals directly in the intestinal

wall, along with amino acid ligands, to which they are bonded.

Dry, by form, is estimated to account for the largest market share

during the forecast period

The dry segment accounted for the

largest share in 2019, as trace mineral products in the dry form enable the

hygienic supply of these ingredients, and the feeding system is comparatively

easy to manage. Furthermore, the ease of mixing dry form of trace minerals into

the total feed, relative cost-effectiveness as compared to the liquid form, and

its long shelf life are some of the other key factors encouraging its use in

dry form. Trace minerals are mostly available in the dry form, as they are easy

to mix with feed products in the appropriate quantity. For instance, the

powdered copper and zinc could be mixed in the ratio of a billion parts of copper

or just one part of zinc. Additionally, other minerals and trace minerals in

powdered form could be mixed in similar ratios, without causing a reaction.

Furthermore, chelated trace minerals in the dry form find application in

various livestock. In addition, when mixed with dry feed, they are often

absorbed more efficiently by the body, if supplied rather than used as

supplements.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=196308436

Asia Pacific is estimated to hold the largest market share during the

forecast period

The trace minerals in feed market

is estimated to grow significantly in the Asia Pacific region due to the rise

in demand for poultry meat and poultry byproducts as well as ruminants from the

major economies such as China, India, Japan and other South East Asian

countries as they experience a surge in the increase in number of health

-conscious consumers. With the increase in awareness amongst consumers about

the essential nutrients requirement in daily diet, have increased the demand

for protein rich meat. In Asia Pacific, trends around healthy lifestyles and

prevention among older consumers trying to avoid expensive healthcare costs and

extend healthy lifespans are generating growth opportunities dietary

supplements. Thus, causing Trace minerals in feed to flourish in the region.

This report includes a study on

the marketing and development strategies, along with a study on the product

portfolios of the leading companies operating in the Trace minerals in feed

market. It consists of the profiles of leading companies such Cargill,

Incorporated (US), (US), BASF SE (Germany), Bluestar Adisseo Co., Ltd (China),

Koninklijke DSM N.V. (Netherlands), Nutreco N.V. (Netherlands), Alltech (US),

Zinpro (US), Orffa (Netherlands), Novus International (US), Kemin Industries,

Inc. (US), Lallemand, Inc. (Canada), Virbac (France), Global Animal Nutrition (US), Dr. Paul

Lohmann Gmbh & Co. KGAA (Germany), Biochem Zusatzstoffe (Germany), Veterinary Professional Services Ltd.

(Vetpro) (New Zealand), Chemlock Nutrition Corporation (US), dr. eckel animal

nutrition gmbh & co.kG (Germany),

Vetline (India), Green Mountain Nutritional Services Inc. (US), Biorigin

(Brazil), Tanke (China), JH Biotech, Inc. (US), QualiTech, Inc. (US)..