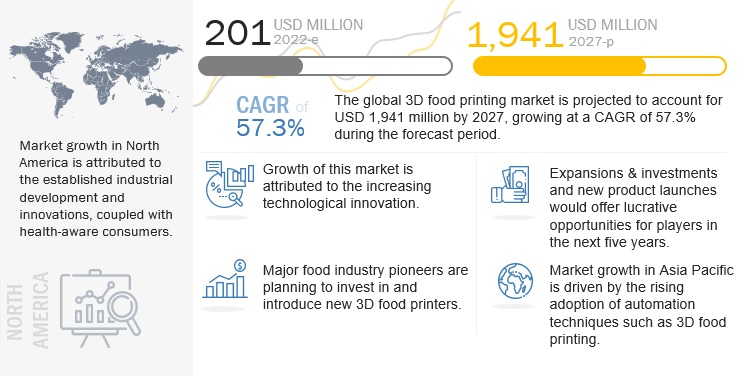

The global 3D food printing market size is estimated to be valued at USD 201 million in 2022 and is projected to reach USD 1,941 million by 2027, recording a CAGR of 57.3% during the forecast period. The demand for 3D food printing is increasing significantly, due to the increasing consumption of customized food products in many countries across the world.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=267692011

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=267692011

Key players in this market include 3D systems (US), TNO (Netherlands), NATURAL MACHINES (Spain), Choc edge (UK), Systems & Materials Research Corporation (US), byFlow B.V. (Netherlands), beehex (US), CandyFab (US), ZMORPH S.A (Poland) and Wiiboox (China). These players have adopted various growth strategies such as partnerships, agreements, and collaborations to increase their presence in the global market.

One of the key players in the global 3D food printing market is byFlow. byFlow is a family business founded in the Netherlands in 2015. It is one of the worlds leading companies in the rapidly growing market of 3D Food Printing. Its mission is to change the way food is prepared and consumed in order to contribute to a more sustainable world. They develop 3D Food Printing Technology, which enables professionals to create customized shapes, textures, and flavors using fresh or otherwise discarded ingredients. Their primary goal is to accelerate the development of innovative 3D Food Printing Technology for a wide range of applications. Their product, the Focus 3D Food Printer, is portable, easy to maintain, and simple to use, making it available to everyone. It is for sale on the open market and is already being used by Top Chefs such as Jan Smink, Caterers, Bakeries, Chocolatiers, and Food Designers who want to experiment with shapes and amaze their customers. Aside from professionals in the food industry, they collaborate with resellers and R&D centers of multinational corporations, looking for further development and applicability of the technology with them. While their primary focus is on selling and developing the Focus 3D Food Printer, they also provide services. In response to the growing interest in 3D Food Printing, we provide demonstrations and workshops at public and private events.

Apart from byFlow, TNO, or the Netherlands Organization for Applied Scientific Research, is also identified as a key player in this market. TNO has been developing expertise in Additive Manufacturing for over 30 years. TNO has created a high-force, high-speed extrusion printing setup that exceeds commercially available limits. Their multi-nozzle printhead platform allows for the simultaneous printing of multiple materials, and their experimental printhead platform investigates the potential of novel extrusion concepts for continuous and large-scale production. Their adaptable powder-bed platform is designed to investigate and print a wide range of liquid and powder classes The company’s core technologies are in ten societal areas Defense, Safety & Security, Artificial Intelligence, Buildings, Infrastructure, and Maritime Circular Economy & Environment Energy Transition Industry, Living a Healthy Lifestyle, Transportation & Traffic, ICT (Information and Communication Technology) and Policy & Strategic Analysis. The company has a presence in Belgium, Japan, and Netherlands.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=267692011

The North America is estimated to account for the largest market share in the 3D food printing market in 2022. The presence and growth of the companies offering the 3D food printing technology in this region are boosting the market in this region. This region is projected to be the largest market during the forecast period.

The US is known as one of the early adopters of the new technologies in the world. The busy and fast-moving life of common people makes it hard for them to get the proper nutritious diet. The 3D food printing technology could provide an option to have customized nutritious food. Also, the US government spends the highest amount of budget on healthcare, and the benefits of 3D food printers to provide food rich in specific nutrients and with the ease of chewing and swallowing would provide a suitable option for feeding the aged patients.