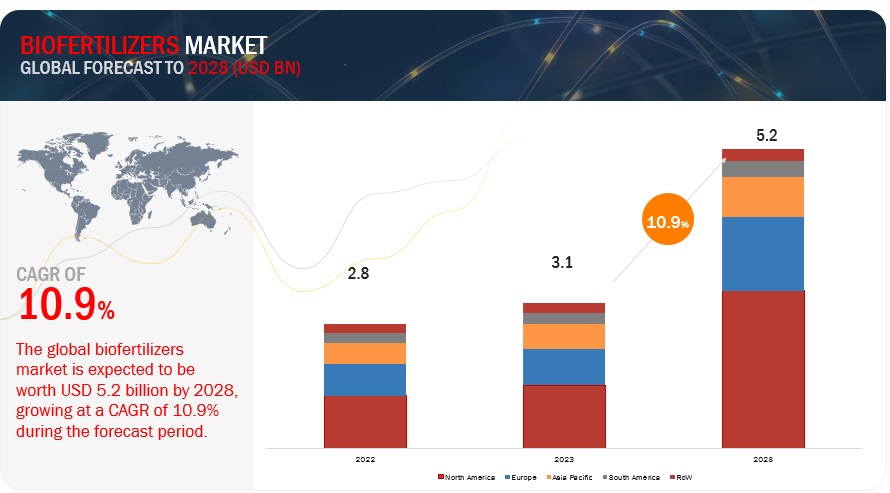

The global biofertilizers market was valued at 2.8 billion in 2022 and is projected to reach 5.2 billion by 2028, growing at a CAGR of 10.9% during the study period. The market is estimated to be valued at USD 3.1 billion in 2023. Through natural processes such as nitrogen fixation, phosphate solubilization, and the production of compounds that stimulate growth, biofertilizers provide nutrients to plants. They boost soil organic matter and aid in restoring the soil's natural nutrition cycle. By using biofertilizers, growers can increase the sustainability and health of the soil and cultivate healthy crops. Only bacteria and other biological elements that are not damaging to the environment are present in biofertilizers. As a result, they contribute to reducing pollution brought on by agricultural activities, particularly soil pollution.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=856

By crop type, fruits & vegetables is forecasted to account for the largest share in the market during the research period

Biofertilizers are known to increase crop productivity of various fruits & vegetables. Fruits such as bananas have a substantial nitrogen requirement, hence the use of biofertilizer, in particular inoculation with Azotobacter, is utilzsed as an alternative and results in a higher yield than full doses of nitrogen administration. In correlation with VAM fungus, there is a rise in the absorption of nutrients that are mobile, such as nitrogen. Organic farming produces high-quality vegetables, thus more farmers are expected to adopt and use microbial biofertilizers in order for modern agriculture to grow sustainably.

Adoption of precision farming and protected agriculture

The goal of precision farming is to produce profitable agricultural output by identifying and analysing spatial and temporal variability using cutting-edge technologies. To boost crop output and yield, agricultural biologicals are employed in precision farming and protected agriculture. The market for biofertilizers is growing as a result of the widespread use of agricultural biologicals in protected agriculture, which promotes the use of biofertilizers. Farmers can track the application of liquid biofertilizer by using fertilisation plans that use GPS-guided geographic information system (GIS) software. Therefore, it is anticipated that the market for biofertilizers will be driven by the rise in land under precision and protected agriculture.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=856

North America is projected to gain the largest market share in the global biofertilizers market.

North America is projected to gain the largest market share in the global biofertilizers market. The presence of large number in the region allows farmers/growers in the region, access to wide range of products at competitive prices. The governments in the region are promoting use of agricultural inputs which causes less environmental degradation and hence are encouraging the use of biofertilizers. In countries such as US and Canada, farmers are focused on producing cash crops at larger scale which is also driving the market in the region.

Key players in this market include Novozymes (Denmark), UPL (India), Chr. Hansen Holding A/S (Denmark), Syngenta (Switzerland), T.Stanes and Company Limited (India), Lallemand Inc (Canada), Rizobacter Argentina S.A. (Argentina), Vegalab SA (Switzerland), IPL Biologicals Limited (India), and Kiwa Bio-tech Product Group Cooperation (China).