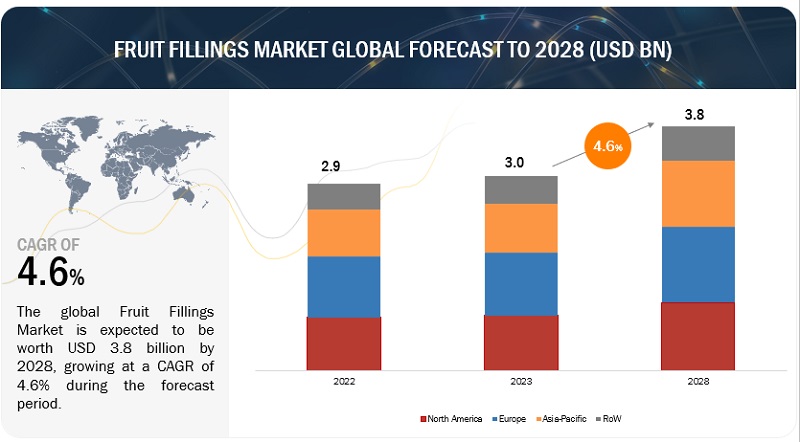

The global fruit fillings market is projected to grow from USD 3.0 billion in 2023 to USD 3.8 billion by 2028, reflecting a CAGR of 4.6% during the forecast period. Rising per capita income and growing health consciousness are driving demand for convenient, flavorful, and natural food options. In the Asia Pacific region, the expanding middle-class population is significantly boosting purchasing power. According to OECD projections, the region could account for 59% of global middle-class consumer spending by 2030. This shift, coupled with increased consumer spending, is fueling demand for natural ingredient-based products like fruit fillings in food and beverages.

Fruit fillings are increasingly preferred as a healthier alternative to artificial sweeteners in bakery and confectionery products. Changing consumer lifestyles and preferences for healthier and flavorful food continue to drive the market.

Fruit Fillings Market Opportunities: Growing Health Awareness Among Consumers

Health and wellness trends are reshaping the food industry, and the fruit fillings market is no exception. Manufacturers are focusing on creating low-sugar, low-fat, and low-calorie fruit fillings while incorporating functional ingredients like dietary fiber to meet consumer demands.

Fruit fillings, rich in vitamins, fiber, and antioxidants, are a natural substitute for refined sugars, making them suitable for individuals managing blood sugar levels or reducing sugar intake. For instance, blueberry fillings are packed with antioxidants, while apple fillings provide dietary fiber. The rising preference for healthier food options is expected to drive the growth of the fruit fillings market.

Expanding Applications in the Dairy Industry

Fruit fillings are extensively used in dairy products like yogurt, cheesecakes, cream cheese spreads, milkshakes, and whipped cream to enhance flavor and texture. American consumers, in particular, are favoring innovative fruit flavors such as peach, passionfruit, guava, and other tropical varieties in cultured dairy products.

As dairy and dairy-alternative categories innovate with nutrient-rich beverages and artisan butter, demand for fruit-based inclusions is increasing. This trend is especially evident in North America, where the growing health-conscious consumer base sees fruit-filled food and beverages as a convenient way to maintain overall health and wellness.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=150631672

United States: A Leading Market in North America

The United States remains a dominant market for fruit fillings in North America, driven by growing consumer health awareness, increasing demand for vitamin C-enriched ingredients, and the preference for natural and flavorful food products.

A wide range of fruit fillings, including berry, apple, citrus, and mixed fruit varieties, are readily available, further fueling market growth.

Leading companies in the fruit fillings market include Puratos Group (Belgium), Dawn Food Products Inc. (US), Agrana Beteiligungs-AG (Austria), CSM Ingredients (Luxembourg), Bakels Worldwide (Switzerland), Barry Callebaut (Switzerland), Andros Group (France), Zentis GmbH & Co. KG (Germany), Rice & Company Inc. (US), and Fruit Filling Inc. (US).

Dawn Food Products, Inc. is a family-owned company specializing in bakery ingredients and solutions, offering products such as bases, mixes, glazes, and fruit fillings. In February 2023, the company expanded its Delifruit range of ready-to-use fruit fillings.

Bakels Worldwide is a global conglomerate in the bakery ingredients industry, producing high-quality fruit fillings in various flavors and textures. In March 2023, Bakels acquired Orley Foods, a provider of sweet ingredient solutions based in Cape Town.

Key Questions Addressed in the Fruit Fillings Market Report:

- What is the current landscape of the fruit fillings market?

- What are the primary applications for fruit fillings?

- What factors are driving market growth?

- What types of fruit fillings are commonly available?

- Which regions lead the fruit fillings market?

- What innovations are influencing the fruit fillings market?

- What are the major growth drivers for the fruit fillings market?

- What is the future outlook for the fruit fillings industry?