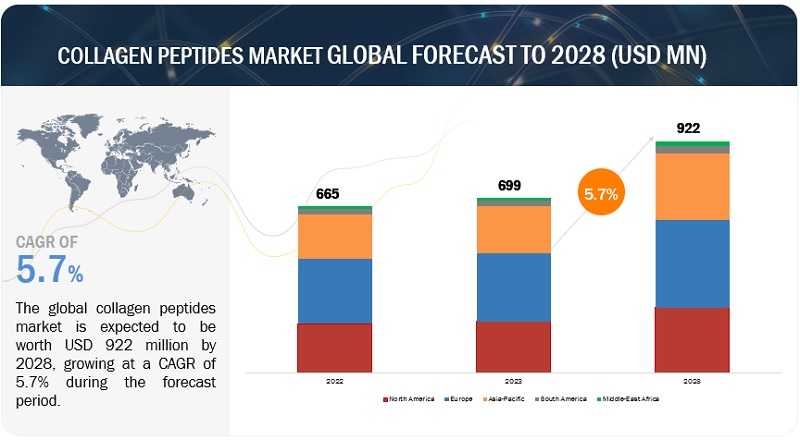

The global collagen peptides market was valued at USD 665 million in 2022 and is expected to grow from USD 699 million in 2023 to USD 922 million by 2028, at a compound annual growth rate (CAGR) of 5.7% from 2023 to 2028. The demand for collagen peptides has surged due to its expanding use across sectors like healthcare, cosmetics, food, and pharmaceuticals. This growth is also supported by increased consumer health awareness in emerging markets, particularly in the Asia Pacific, Middle East, Africa, and South America regions.

Collagen Peptides Market Drivers: Rising Demand in Cosmetics and Personal Care

Collagen plays a crucial role in skin structure, but as people age, the collagen fibers in the skin weaken, leading to reduced thickness and elasticity. This results in the visible signs of aging. Collagen peptides are increasingly used in cosmetics and personal care products, such as creams, shampoos, body lotions, facial creams, and soaps. These peptides are also used as nutritional supplements to support bone health and in skin replacements to enhance skin texture. In the cosmetic industry, collagen peptides are utilized for soft tissue augmentation, cosmetic surgery, and skin rejuvenation treatments. They are commonly used in dermal fillers to restore facial volume and improve facial contours. With a globally aging population and rising per capita incomes, the demand for collagen peptides in cosmetics and personal care products is expected to continue growing.

Technological Advancements in Extraction and Production

Recent technological advancements have significantly improved collagen extraction and production processes. Traditional methods, like boiling or acid treatment, have been optimized, while modern techniques like enzymatic hydrolysis—where specific enzymes break down collagen into smaller peptides—offer greater efficiency and higher-quality peptides. These advancements have broadened the range of collagen sources and allowed for tailored products to meet diverse dietary needs. Additionally, improved purification and concentration techniques ensure that collagen peptides maintain high purity and consistent molecular weight, contributing to their effectiveness.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248590980

Growing Consumer Health Awareness and Food & Beverage Use

Collagen peptides are increasingly incorporated into a wide range of food and beverage products, including functional foods, dietary supplements, sports nutrition, and therapeutic foods. Their versatility as an ingredient is driving their use across various sectors, especially in dairy products, where collagen peptides are prized for their clean label appeal. Collagen peptides offer multiple health benefits, such as supporting muscle, tendon, ligament, and cartilage repair, making them popular in sports nutrition. They also help alleviate post-exercise joint pain and enhance joint and ligament strength. As more consumers focus on health and wellness due to changing lifestyles, the demand for collagen peptides, particularly in dietary supplements, is expected to grow, further boosting market expansion.

Europe's dominance in the Collagen Peptides Market Share.

Europe is anticipated to lead the collagen peptides market throughout the forecast period. Countries like Germany, the UK, France, Italy, and Spain are seeing strong demand, driven by high consumer awareness of health and a robust cosmetics and personal care industry. France, in particular, is renowned for its cosmetics sector, which is highly innovative and research-focused. Additionally, Europe is a major hub for the pharmaceutical industry, further driving the use of collagen peptides in biomedical applications.

Leading Collagen Peptides Manufacturers

Several key players are based in Europe, including Gelita AG (Belgium), Tessenderlo Group (Belgium), and Lapi Gelatine S.p.A. (Italy), making the region critical to the collagen peptides market. Other global players like Nitta Gelatin Inc. (Japan), Holista Colltech (Australia), Darling Ingredients (US), and Foodmate Co., Ltd. (China) also contribute to the region’s market presence. The study includes an in-depth competitive analysis of these companies, examining their profiles, recent developments, and market strategies.