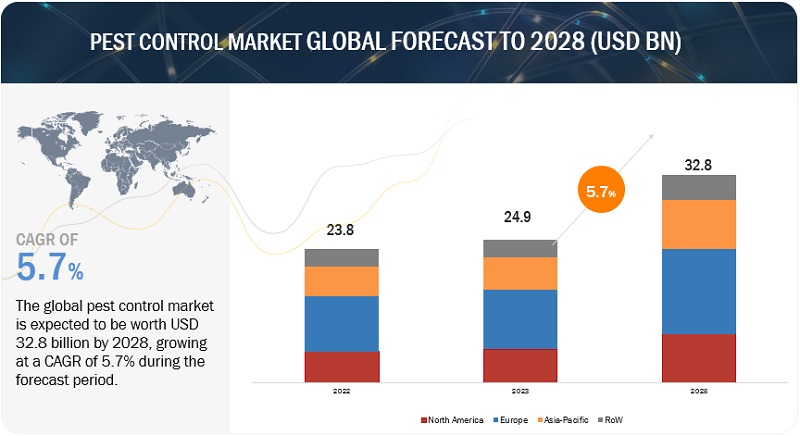

The pest control market size is projected to reach $32.8 billion by 2028 from an estimated $24.9 billion in 2023, at a CAGR of 5.7% during the forecast period in terms of value. Several important factors are augmenting the demand for pest control products and services on a global scale. Increasing awareness of the health risks posed by pests and the diseases they can transmit is driving individuals and businesses to prioritize pest prevention and control. This heightened concern for health and hygiene fuels the demand for pest control services. Moreover, advancements in pest control technologies and methods have improved the efficacy, precision, and sustainability of treatments, making them more appealing to consumers.

Pest Control Market Share:

The key players in this include Bayer AG (Germany), Corteva Agriscience (US), BASF SE (Germany), Sumitomo Chemical Co. Ltd. (Japan), Syngenta AG (Switzerland), Rentokil Initial plc (UK), Anticimex (Sweden), Rollins, Inc. (US), ATGC Biotech Pvt Ltd. (India), Ecolab Inc. (US), FMC Corporation (US), De Sangosse (France), Bell Laboratories (US), PelGar International (UK), and Fort Products Limited (UK).

Pest Control Market Trends

- Sustainability: With increasing environmental concerns, there's a growing demand for eco-friendly pest control solutions. This includes the use of organic products, non-toxic methods, and sustainable practices to minimize harm to the environment.

Integrated Pest Management (IPM): IPM continues to gain traction as a comprehensive approach to pest control. It emphasizes prevention, monitoring, and control, reducing reliance on chemical treatments and promoting long-term solutions.

Technology Integration: Advancements in technology are revolutionizing pest control. From smart traps and sensors to data analytics and remote monitoring systems, technology is enhancing efficiency, accuracy, and predictive capabilities in pest management.

Focus on Health and Safety: Consumers are increasingly prioritizing health and safety concerns, driving the demand for pest control methods that are safe for humans and pets. This includes the use of low-toxicity products and application techniques that minimize exposure risks.

Rise of Professional Services: While DIY solutions remain popular for minor pest problems, many consumers are turning to professional pest control services for more challenging infestations. Professional expertise, specialized equipment, and guaranteed results are key factors driving this trend.

Urbanization and Pest Pressure: As urban areas continue to expand, pest pressure is on the rise. This trend is fueling the demand for proactive pest control measures in both residential and commercial settings, driving market growth.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=144665518

North America is expected to have the largest market share during the forecast period.

The market for pest control is growing in North America owing to the widening scope of applications in not only residential or commercial but also in livestock and for industrial purposes, such as in the food and pharmaceutical industries. The pest control market in North America is experiencing notable growth owing to a convergence of factors. Moreover, there are numerous companies in North America providing pest control products and services. Apart from major players, there are many local players in the market. The presence of numerous pest control companies in the region also indicates that there is high demand for the pest control management. Stringent regulations in industries such as food safety and hospitality further bolster the market's expansion. Innovations in pest control technologies, including eco-friendly solutions and integrated approaches, enhance efficacy and appeal to environmentally conscious consumers.