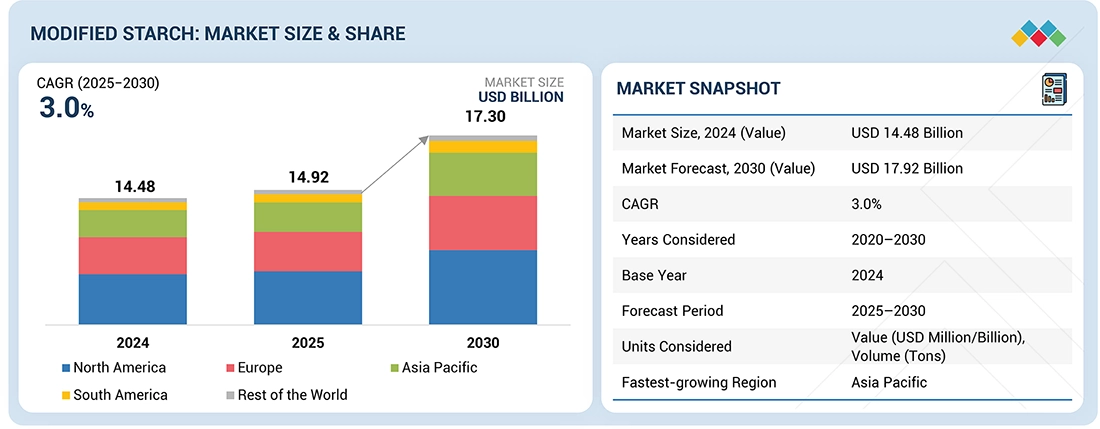

The global modified starch market is valued at USD 14.92 billion in 2025 and is projected to reach USD 17.30 billion by 2030, growing at a CAGR of 3.0%. Market expansion is driven by the rising focus on product stability, texture improvement, and clean-label functionality across processed and convenience food categories. As consumers increasingly prefer healthier, high-quality, and easy-to-use food products, demand for transparent and natural ingredient solutions has surged—strengthening the adoption of modified starches in multiple applications.

A growing shift toward functional, science-backed ingredients that enhance viscosity, binding, freeze–thaw stability, and overall performance is further accelerating market growth.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=511

Dominance of Physically Modified Starch

The physically modified starch segment is expected to hold the largest market share during the forecast period. This category has gained strong traction because it supports the global trend toward clean-label, natural, and minimally processed ingredients while still offering robust functional benefits.

Produced through non-chemical processes such as heat–moisture treatment, pregelatinization, annealing, extrusion, and spray drying, physically modified starch enhances key properties like solubility, viscosity, water absorption, and freeze–thaw stability—without the use of chemical agents. This enables simpler ingredient labeling, which appeals to health-conscious consumers and aligns with stringent regulatory standards in regions such as Europe and parts of Asia.

Moreover, physically modified starches offer cost-efficient production, easy scale-up, and versatile formulation capabilities across bakery, dairy, snacks, instant foods, gluten-free items, pharmaceuticals, and industrial applications. Their reliability, consistency, and regulatory compliance continue to position them as the preferred choice across both food and non-food sectors.

Dry Form Leads Market Adoption

The dry form of modified starch is projected to account for a significant market share due to its superior stability, long shelf life, and convenient storage and transportation. Its powdered form enables accurate dosing, simple handling, and seamless blending across food and industrial processes.

Widely utilized in bakery mixes, instant foods, snacks, adhesives, paper applications, and pharmaceuticals, dry modified starch is favored for its compatibility with high-temperature and high-shear environments. Reduced logistics costs, minimal spoilage risks, and broad functional versatility continue to make dry starch the most preferred format globally.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=511

Asia Pacific: The Fastest-Growing Regional Market

Asia Pacific is poised to remain the fastest-growing region in the modified starch market, supported by a strong agricultural foundation, rapid industrialization, and a booming food processing sector. Countries such as China, India, Thailand, Indonesia, and Vietnam benefit from abundant raw materials—including cassava, corn, and potatoes—providing the region with a significant production and cost advantage.

Urbanization, evolving lifestyles, and increasing consumption of processed and convenience foods continue to drive modified starch demand in bakery, dairy, snacks, and ready-to-eat products. Additionally, rising applications in pharmaceuticals, textiles, adhesives, and paper manufacturing are accelerating regional growth. Government initiatives promoting agri-processing and bio-based industries, along with strategic investments by global and local manufacturers in R&D, new facilities, and partnerships, further strengthen the region’s market dominance.

Leading Modified Starch Companies:

The report profiles key players such as ADM (US), Cargill (US), Ingredion (US), Tate & Lyle (UK), Roquette Frères (France), Avebe U.A. (Netherlands), Grain Processing Corporation (US), Emsland (Germany), AGRANA (Austria), SMS Corporation (Thailand), Global Bio-Chem Technology Group (Hong Kong), SPAC Starch (India), Qingdao CBH Company (China), Tereos (France), and KMC (Denmark).