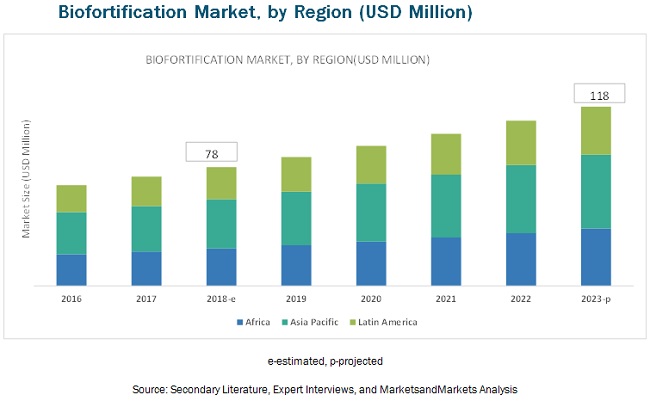

The report “Biofortification Market by Crop (Sweet Potato, Cassava, Rice, Corn, Wheat, Beans, and Pearl Millet), Target Nutrient (Zinc, Iron, and Vitamins), and Region (Latin America, Africa, and Asia Pacific) – Global Forecast to 2023 “, is estimated at USD 78 million in 2018, and it is projected to grow at a CAGR of 8.6% from 2018 to reach USD 118 million by 2023. Biofortified crops are usually sweet potato, cassava, rice, corn, wheat, beans, pearl millet, and other crops such as tomato, banana, sorghum, and barley. The growth of the biofortification market is driven by the rising demand for high nutritional content in food.

By crop, the biofortified sweet potato is projected to dominate the biofortification market during the forecast period.

The sweet potato segment is estimated to hold the largest share of the biofortified crop market in 2018. The demand for biofortified crops such as sweet potato and cassava has increased with the rising technological advancements to increase the nutrient content, particularly in orange-fleshed sweet potato (OFSP). Sweet potato has been an important source of energy in the human diet for centuries owing to its high carbohydrate content. However, its vitamin A content from carotene only became recognized over the past century. Using biofortification, sweet potato breeding in Africa is focused on higher yields, sweeter taste, and higher dry matter, which increase its carotene concentration.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38080924

By target nutrient, the vitamins segment is projected to be the fastest-growing segment in the biofortification market during the forecast period.

On the basis of target nutrient, the biofortification market is segmented into iron, zinc, vitamins, and others. The vitamins segment is the fastest-growing target nutrient in the biofortification market from 2018 to 2023. The demand for biofortified crops is increasing due to the increasing demand for high nutrient content in food. The rising demand for vitamins as feed additives or in premixes from the animal nutrition industry and the increasing demand for high-quality meat products have also been essential factors responsible for the increase in the demand for vitamins across the world.

Asia Pacific to be the dominant region in the biofortification market in 2018

The Asia Pacific is the dominant region in the biofortification market. Biofortification of crops has strong growth potential in agriculture, and it also improves the nutrition content in food. The biofortification market has grown considerably over the last five years, and this trend is expected to continue in the near future. The growing consumer demand for high nutritional content in food is projected to fuel the demand for biofortified crops, globally. Since the last decade, many countries in the Asia Pacific region have banned the usage of GM technology, and the researchers are opting to adopt biofortified crops as a key to unlock the region’s food production.

This report includes a study of marketing and development strategies along with the product portfolios of the leading companies in the biofortification market. It also includes the profiles of leading companies such as Bayer (Germany), Syngenta (Switzerland), Monsanto (US), and DowDuPont (US).

Request for Customization: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=38080924

By crop, the biofortified sweet potato is projected to dominate the biofortification market during the forecast period.

The sweet potato segment is estimated to hold the largest share of the biofortified crop market in 2018. The demand for biofortified crops such as sweet potato and cassava has increased with the rising technological advancements to increase the nutrient content, particularly in orange-fleshed sweet potato (OFSP). Sweet potato has been an important source of energy in the human diet for centuries owing to its high carbohydrate content. However, its vitamin A content from carotene only became recognized over the past century. Using biofortification, sweet potato breeding in Africa is focused on higher yields, sweeter taste, and higher dry matter, which increase its carotene concentration.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=38080924

By target nutrient, the vitamins segment is projected to be the fastest-growing segment in the biofortification market during the forecast period.

On the basis of target nutrient, the biofortification market is segmented into iron, zinc, vitamins, and others. The vitamins segment is the fastest-growing target nutrient in the biofortification market from 2018 to 2023. The demand for biofortified crops is increasing due to the increasing demand for high nutrient content in food. The rising demand for vitamins as feed additives or in premixes from the animal nutrition industry and the increasing demand for high-quality meat products have also been essential factors responsible for the increase in the demand for vitamins across the world.

Asia Pacific to be the dominant region in the biofortification market in 2018

The Asia Pacific is the dominant region in the biofortification market. Biofortification of crops has strong growth potential in agriculture, and it also improves the nutrition content in food. The biofortification market has grown considerably over the last five years, and this trend is expected to continue in the near future. The growing consumer demand for high nutritional content in food is projected to fuel the demand for biofortified crops, globally. Since the last decade, many countries in the Asia Pacific region have banned the usage of GM technology, and the researchers are opting to adopt biofortified crops as a key to unlock the region’s food production.

This report includes a study of marketing and development strategies along with the product portfolios of the leading companies in the biofortification market. It also includes the profiles of leading companies such as Bayer (Germany), Syngenta (Switzerland), Monsanto (US), and DowDuPont (US).

Request for Customization: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=38080924

Key Questions Addressed by the Report:

- What are the new target nutrients areas, which the biofortification companies are exploring?

- Which are the key players in the market and how intense is the competition?

- What kind of competitors and stakeholders such as biofortification companies, would be interested in this market? What will be their go-to strategy for this market and which emerging market will be of significant interest?

- How are the current R&D activities and M&As for biofortified crop industry projected to create a disruptive environment in the coming years for the agricultural sector?

- What will be the level of impact on the revenues of stakeholders through the benefits of nanotechnology to different stakeholders‒‒from rising farmer revenue to environmental regulatory compliance to sustainable profits for the suppliers?