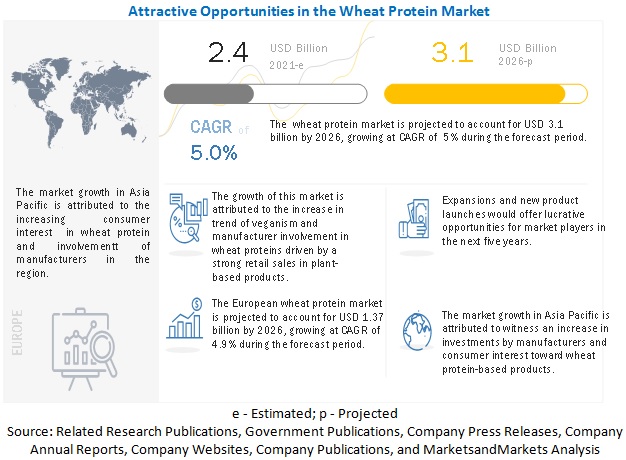

The report "Wheat Protein Market by Product (Wheat Gluten, Wheat Protein Isolate, Textured Wheat Protein, Hydrolyzed Wheat Protein), Application (Bakery, Pet Food, Nutritional Bars, Processed Meat, Meat Analogs), Form (Dry, Liquid), and Region - Global Forecast to 2026", The wheat protein market is projected to reach USD 3.1 billion by 2026, from USD 2.4 billion in 2021, at a CAGR of 5.0% during the forecast period. The market is driven by factors such as a shift in preference for plant-based protein foods, increased demand for meat-free diets, and growing incidence of lactose intolerance.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=67845768

COVID-19 impact on Wheat Protein market

The COVID-19 pandemic has had a profound impact on the wheat protein market. Given the growing consumer awareness of the impact of the pandemic on meat production, consumers began adopting plant-based alternatives instead. This resulted in a sales surge of over 500% for meat alternative brands. The pandemic has also influenced the sales of plant-based snacks, dairy alternatives, and supplements, as consumers move towards a healthier lifestyle.

Driver: Nutritional benefits for lactose intolerant and health- & fitness-conscious consumers

The Lactose intolerance is defined as a condition whereby, the body cannot easily digest lactose, which is a type of natural sugar found in milk and other dairy products. Although some people having a lactose intolerance issue are able to digest whey protein isolates, without any severe repercussions, others find it easier to digest only plant-based proteins. Although whey protein isolates are further processed and filtered to help eliminate more lactose in comparison to whey protein concentrates, any individual with even a mild intolerance towards lactose should avoid the consumption of these products. In such cases, plant-based alternatives stand as the most suitable option, for those looking to increase protein intake, for health or training purposes. A number of plant-based alternatives, which could be used in place of whey proteins include pea protein isolates, brown rice protein, or wheat protein.

Challenges: Limited technological developments

Although the market for wheat protein is expected to witness progressive growth rates during the forecast period, limited technological developments in the market are expected to hinder higher growth rates. While related industries like those of whey protein and the market for gluten-free products are expected to invest substantially in research & development activities to develop better, convenient, and more consumer-suitable products, technological advancements in case of wheat proteins remain stunted. For example, FrieslandCampina DMV recently launched a new product called the Nutri Whey Hydro during Fi Europe 2017. This product was created by working on a specific and unique protein hydrolyzation process that was gentle in nature and helped optimize the taste and nutrition of the product simultaneously. Although the hydrolyzed protein market is expected to be gaining traction during the forecast period, one of the major challenges that the market faces, is its bitter and unpleasant taste. By advancing in new technological methods to optimize tastes and nutritional capabilities, the company has now successfully mitigated that challenge.

By product, wheat gluten segment is projected to dominate the market during the forecast period.

The wheat protein market has been segmented into wheat gluten, wheat protein isolate, textured wheat protein, and hydrolyzed wheat protein. Wheat gluten dominated the global market, in terms of both, value and volume. The wide range of functionalities of wheat gluten such as viscoelasticity, texturing, foaming, emulsification, and binding leads to its wide-scale usage in bakery products. Its role as an excellent meat alternative for consumers preferring vegetarian food products is expected to drive its demand during the forecast period.

Request for Customization:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=67845768

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=67845768

Asia Pacific is projected to. be the fastest-growing region in the wheat protein market during the forecast period.

The Asia Pacific region is projected to be the fastest-growing region due to increased demand for meat-free diets and a shift in consumer preference for healthy food options. The increase in R&D for plant-based protein, the growing vegan population, new product launches, and growing investments in the bakery industry are expected to drive the market growth in this region during the forecast period.

Key Market Players:

Key players in this market include ADM (US), Cargill (US), Agrana (Austria), MGP Ingredients (US), Manildra Group (Australia), Roquette (France), and Glico Nutrition (Japan). These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific, and Europe. They also have manufacturing facilities, along with strong distribution networks across these regions.