The report "Functional

Proteins Market by Type (Whey Protein Concentrates, Isolates, Hydrolysates,

Casein, Soy Protein), Source (Animal, Plant), Form (Dry, Liquid), Application

and Region – Trends and Forecast to 2025" According to

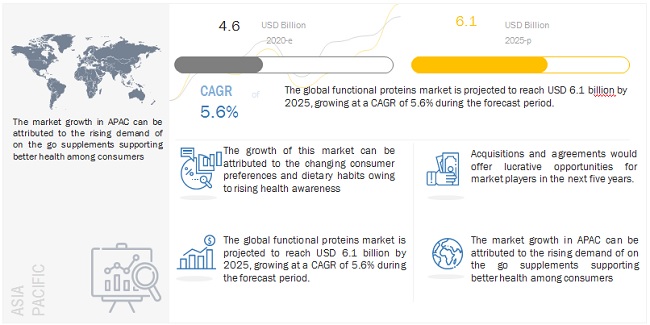

MarketsandMarkets, the global functional proteins market size is estimated to

be valued at USD 4.6 billion in 2020 and projected to reach USD 6.1 billion by

2025, recording a CAGR of 5.6% during the forecast period.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=140299581

The demand for functional proteins is increasing

significantly owing to the shift in consumers’ food-related preferences and

rising prevalence of chronic diseases. Rising health awareness and increase in

disposable income across the globe are key factors that are driving the growth

of the functional proteins market. The millennial population is capturing a

large share of the market as the ongoing health and wellness trend ergo the

surging internet penetration is altering consumer preferences and moving

towards adapting protein-infused functional foods into their diets in order to

maintain quality of life.

The functional food

segment, by application, is projected to witness significant growth during the

forecast period.

The deficiency of proteins in adults is one of the key

factors that have led to the rise in the consumption of functional food

products among adults. This deficiency is mainly due to the untimely schedules

and hectic lifestyles of comsumers, which leads to unhealthy eating habits and

irregular diets. As a result, there is a demand for healthy, on-the-go

functional food products which significantly reduce consumption time while

providing essential nutrition.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=140299581

The North American

region dominates the functional proteins market with the largest share in 2020.

North America is projected to hold the largest share in the

functional proteins market. This dominance is driven by the prevalence of

chronic diseases due to the hectic lifestyles and increasing awareness among

consumers regarding the health benefits of consuming functional proteins. Also,

obesity is on the rise among the North American population, especially the US.

According to the CDC, in the US, the obesity prevalence was 39.8% and affected

about 93.3 million adults between 2015 and 2016. Such factors are projected to

drive the growth of the functional proteins market.

This report includes a study on the marketing and development strategies, along with the product portfolios of leading companies. It consists of profiles of leading companies, ADM (US), DuPont (US), Cargill (US), Ingredion (US), Arla Foods (UK), Roquette (France), BASF (Germany), Glanbia (Ireland), Fonterra (New Zealand), DSM (Netherlands), FrieslandCampina (Netherlands), Essentia Protein Solutions (UK), Amai Proteins (Israel), Mycorena (Sweden), Merit Functional Foods (Canada), Plantible Foods (US), BENEO (Germany), ProtiFarm (Gelderland), and Omega Protein (US).