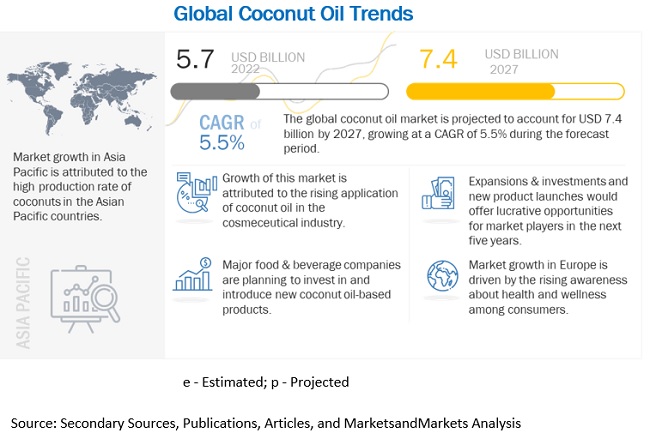

The report "Coconut Oil Market by Product Type (RBD, Virgin, and Crude), Source (Dry Coconut and Wet Coconut), Application (Food & Beverages, Cosmetics & Personal Care Products, and Pharmaceuticals), Nature and Region - Global Forecast to 2027", is estimated to be valued at USD 5.7 billion in 2022. It is projected to reach USD 7.4 billion by 2027, recording a CAGR of 5.5% during the forecast period. The global coconut oil market has been influenced by some of the macroeconomic and microeconomic factors witnessed in some key countries. This would prove strong enough to drive the market significantly in terms of value sales during the forecast period. With the rise in demand and preference for natural cosmetic ingredients, the trend of clean-label and plant-based products has significantly boosted the utilization of coconut oil derivatives in the food industry. Coconut oil is used as a thickener and binder, and this enhances its properties, such as smoothness, hardness, gloss, and whiteness.

Download PDF Brochure

@

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=78320975

Pharmaceutical market is a relatively untapped and small market in

comparison to other non-food applications and the rapidly growing food &

beverage market.

Coconut oil is used as one of the components of cosmetic ingredient, majorly as a smoothening agent and as a source of smooth skin and to improve the dryness of skin and hairs. Companies are focusing on the development of extraction and processing of coconut oil to discover new beauty applications. Coconuts are the primary source of coconut oil. Coconut oil in food and beverages acts as a cooking oil replacer in order to enhance the flavor. It is a source of carbohydrates, which helps in improving digestibility.

Increasing use of Coconut oil in bakery products

Coconut oil is gaining popularity in the US due to several health benefits offered by it; it helps in reducing weight, strengthening the immune system, preventing heart disease, and staving off dementia and Alzheimer’s disease. In the food industry, coconut oil is used extensively in baked products, processed foods, and infant formulas. The use of organic coconut oil in the bakery coupled with the increasing growth of the bakery industry is projected to propel the demand for coconut oil.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=78320975

North America is expected to be the third largest market during the

forecast period.

North American coconut oil market is completely driven by the US market. The US coconut oil industry has witnessed technological advancement, which has increased its usage in various industries. In the US, coconut oil is primarily used in organic form in the confectionery products a s a health beneficial. It is also used as a base for gelling agents in confections, for thickeners in products such as pastry and pie fillings, and in instant puddings. The growing trend of ready-to-eat meals and processed food is also driving the coconut oil market in the region. Coconut oil is frequently used in food applications due to its functional properties.

The key players in this market include Tate & Lyle (UK), Emsland (Germany), Ingredion Incorporated (US), and Avebe (Netherlands).