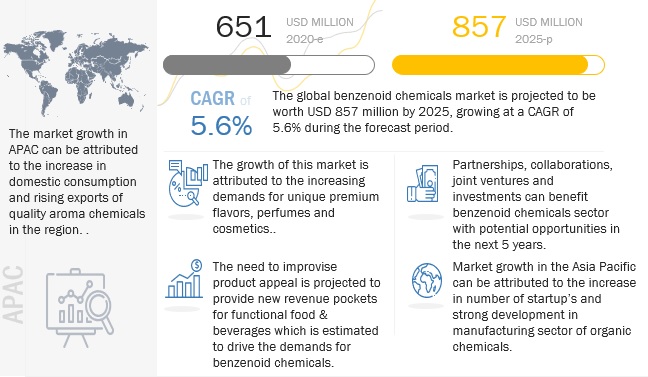

The report "Benzenoid Market by Type (Benzyl Acetate, Benzoate, Chloride, Salicylate, Benzaldehyde, Cinnamyl, Vanillin), Application (Soaps & Detergents, Food & Beverage, Household Products), and Region – Global forecast to 2025", size is estimated to be USD 651 million in 2020 and is projected to reach USD 857 million by 2025, at a CAGR of 5.6% during the forecast period. The market is being strongly driven by soaps & detergents industry, which is witnesses a high demand. With newer premium products coming up in the market and unique fragrance blends, their demand is projected to grow in the market in the near future

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=18857610

The spread of COVID-19 pandemic affected the overall chemicals market in the global regions. The value of trade in organic chemicals reached USD 846 billion in 2019, which decreased by nearly 10% from 2018 in terms of value. The economy of China was also affected by events such as the Chinese economic slowdown & US-China trade wars. As reported by the Financial Express in May 2020, the country recorded low oil prices in 2020 and has impacted the chemicals and petrochemicals industries. The low demand for fuels due to the lockdown has led to the low production of many chemicals. The major benefitting end use sector for benzenoids chemicals, such as cosmetics, fine fragrances, and perfumes, were majorly impacted. There are over 1,000 small, medium, and large-size enterprises operating in this industry, both in the organized and unorganized sector, and almost all the food, pharma, FMCG industries are dependent on fragrances and flavors. However, with reopening markets and economies show that the business are recovering soon and the market is estimated to regain their business after alockdowns end.

The soaps and detergents sub-segment, in by application segment , is

projected to dominate the market during the forecast period.

The demand for soaps and detergents have been observing a stable demand from the global market in the pre-Covid period and their demands, further spikes since thre spread of Covid-19 with the increasing focus of the population on cleanliness and hygiene. For these, there were rising demand for production of quality and premium fragrance products. These are estimated to drive the market growth.

The benzyl benzoate sub-segment, in the by type, is projected to

witness the highest growth in the benzenoids market

Benzyl benzoate is estimated to observe the fastest market growth during the forecast period in the benzenoids market as the compound is a thick liquid that has a weak, sweet-balsamic odor and it occurs naturally in some flower blossoms, fragrances and benzyl benzoate can also be formulated in a lab with added scents to slow their evaporation. It serves a supporting role that helps in dissolving and blending together all the different scent substances. Thus their usage is expected to grow.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=18857610

Asia Pacific is estimated to be the largest market.

The Asia Pacific region is estimated to account for the largest share of the global benzenoids market in 2020. The rising income, purchasing power, rapid growth of the middle-class population, and consumer demand for processed products present promising prospects for growth and diversification in the region’s benzenoids sector. The European aroma chemicals manufacturers are gradually losing their market share, failing to compete with products from Asia (mainly from China), where labor costs are much lower and the quality control is constantly growing, imitating western technologies. Further, countries such as China, Japan, South Korea, and Indonesia are witnessing significant growth in the cosmetics, beauty, and personal care products markets. These rae expected to drice the growth from benzenoid chemiclas in the region.

Key players in this market include include major players such as BASF (Germany), Firmenich (Switzerland), Emerald Kalama Chemical (US), International Flavors & Fragrances, Inc. (US), Eternis Fine Chemicals (India), Symrise (France), Tennants Fine Chemicals Ltd. (England), Jayshree Aromatics Pvt. Ltd. (India), and Valtris Specialty Chemicals (US. These major players in this market are focusing on increasing their presence through expansions & investments, mergers & acquisitions, partnerships, joint ventures, and agreements. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.