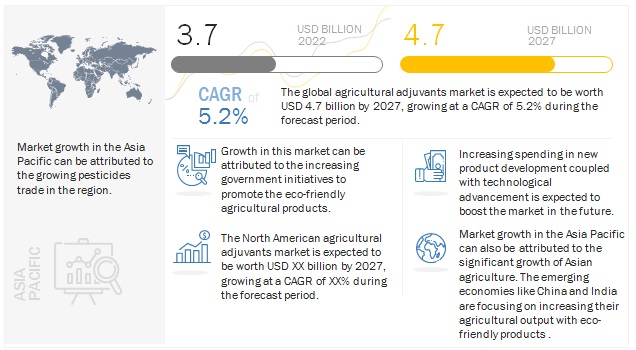

According to MarketsandMarkets, the Agricultural Adjuvants Market size is estimated to be valued at USD 3.7 Billion in 2022 and is projected to reach USD 4.7 Billion by 2027, recording a CAGR of 5.2% during the forecast period in terms of value. The agricultural adjuvants market is expected to witness significant growth due to factors such as the growing demand for sustainable agricultural practices, the increasing harvested area of industrial and high-value crops, and a surge in the number of investments from key players in this market. The increasing use of crop protection chemicals in developing countries to combat pest attacks encourages manufacturers to develop in-formulation adjuvants suitable for these regions. Key players such as Evonik Industries, Clariant, and Solvay focus on developing multifunctional adjuvants that cater to various applications.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1240

The US and Canada are the primary consumers of pesticides in the North American region. Also, the adoption rate of modern agricultural practices in the US is higher than in Canada and Mexico. Due to the increasing presence of production facilities by prominent players for adjuvants in the US, the consumption of agricultural adjuvants in terms of volume is projected to remain higher in this country than in the other two. However, due to the growing agricultural industry in Canada and the rising adoption rate of efficient agricultural inputs to reap maximum crop output, Canada is expected to register the highest growth among the three North American countries.

Based on function, the utility adjuvants segment is projected to dominate the agricultural adjuvants market in the forecasted period. The demand for utility adjuvants remains high in developed countries due to the introduction of strict regulations on pesticide usage and increasing government support for a sustainable foliar spray of pesticides. However, due to their high cost, the adoption of adjuvants in developing countries is low. Hence, utility adjuvants are projected to offer lucrative growth opportunities for manufacturers in developed countries during the forecast period.

Among various adoption stages, tank-mix agricultural adjuvants are anticipated to witness the highest growth rate over the forecast period. The addition of tank-mix adjuvants is preferred for applications such as aerial spray and low-volume spray, as it offers optimal performance. Many companies are investing in R&D activities for developing environment-friendly and effective tank-mix adjuvant solutions.

Based on application, the herbicides segment is projected to dominate the agricultural adjuvants market. Adjuvants are widely used in spray mixtures with pre-plant burndown or in-crop post-emergence (POST) herbicide applications. Pre-emergent herbicides help in preventing weeds from long-term growth, and post-emergent herbicides work on the already grown weeds. Post-emergent herbicides are the most popular substances in weed control.

Among various crop types, fruits & vegetables is estimated to witness the highest growth rate during the forecasted period. Fruits and vegetables have become an indispensable part of daily diets, particularly with the growing awareness regarding their nutritive value. The consumption of fruits has witnessed a significant increase in the past two decades, and this trend is projected to continue in the coming years.

Based on formulation type, suspension concentrates is estimated to hold the largest market share in 2022. Suspension concentrates (SCs) are the most preferred end-product formulations in the market because they are safer to use on crops than emulsifiable concentrates. This is a key factor driving market growth in the coming years.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=1240

This report includes a study on the marketing and development strategies, along with the product portfolios of leading companies. It consists of profiles of leading companies, such as Corteva Agriscience (US), Evonik Industries (Germany), Croda International (UK), Nufarm (Australia), Solvay (Belgium), BASF SE (Germany), Huntsman Corporation (US), Clariant AG (Switzerland), Helena Agri-Enterprises LLC (US), Stepan Company (US), Adjuvant Plus Inc. (Canada), Wilbur-Ellis Company (US), Brandt, INC. (US), Plant Health Technologies (US), Innvictis Crop Care LLC (US), Miller Chemical And Fertilizer, LLC (US), Precision Laboratories, LLC (US), CHS Inc. (US), Winfield United (US), KaloInc. (US), Nouryon (Netherlands), Interagro Ltd. (UK), Lamberti S.P.A (Italy), Garrco Products, Inc. (US), Drexel Chemical Company (US), and Loveland Products Inc. (US).