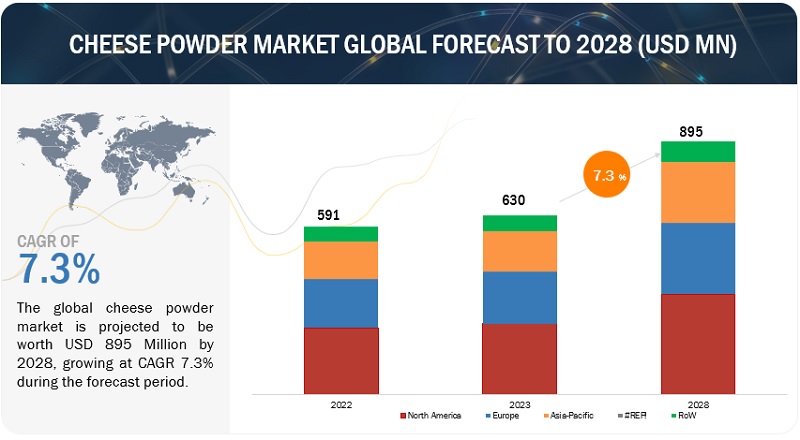

According to a research report "Cheese Powder Market by Type (Cheddar, Mozzarella, American Cheese, Blue Cheese, Parmesan), Application (Bakery & Confectionery, Sweet & Savory Snacks, Sauces, Dressings, Dips, and Condiments, Ready Meals), Origin and Region - Global Forecast to 2028" published by MarketsandMarkets, the global market for cheese powder was valued at USD 630 million in 2023 and is projected to reach USD 895 million by 2028, at a CAGR of 7.3 % during the forecast period. The increasing demand for convenience foods is one of the major drivers of the cheese powder market. The major industrial users of cheese powders include producers of snacks, soups, sauces, frozen products, and ready-to-eat meals. Snacks is the major application of cheese powder due to its easy handling and longer shelf life. Its use in dry snacks has been largely contributing to the growth of the market.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=103908380

Cheddar cheese powder in by type segment accounted for the largest share of the cheese powder in 2023 in terms of value.

Cheddar is one of the most popular and widely consumed cheese varieties, and its trends often reflect broader developments in the cheese powder industry. Cheddar is a relatively hard natural cheese and is off-white in color. It is the most widely used type of cheese for the manufacturing of cheese powders. Cheddar cheese powder has low calorie, saturated fat, salt, and cholesterol content. This has led to an increase in demand for cheddar cheese powder in North America owing to the rising health-consciousness among people. Moreover, consumers showing increased interest in high-quality, artisanal, and premium cheddar cheeses. These offerings often came from small-scale producers and were appreciated for their unique flavors and production methods.

Processed cheese powder in by origin segment accounted for the largest share of the cheese powder in 2023 in terms of value.

Processed cheese products are widely used in the foodservice industry, including quick-service restaurants and casual dining establishments, due to their convenience and ease of use in various menu items. Processed cheese was used as a key ingredient in snack products, such as cheese crackers and cheese snacks. The growth of the snack industry and the demand for savory, flavorful snacks were contributing to the processed cheese market. Moreover, processed cheese products are more cost-effective than natural cheeses, making them a budget-friendly option for both consumers and foodservice establishments.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=103908380

Ready meals in the application segment is estimated to grow at the highest in the cheese powder market.

Cheese powder is used in ready meals to add a specific cheese’s flavor to the meal or to enhance the existing flavor in it. With the growingly busy lifestyles of consumers, the popularity of ready meals is rising in developed countries such as the U.S., Germany, and the U.K., among others. This boosts the demand for cheese powder in ready meals across regions. Moreover, ready meal manufacturers are incorporating cheese powder from different cuisines to create fusion dishes that offered a blend of flavors. For example, cheese in Asian-inspired dishes or Mexican-style meals. Ready meals inspired by international cuisines are incorporating cheeses unique to those regions. This trend catered to consumers' growing interest in global flavors.

The North American region is expected to grow at a significant rate in the global cheese powder market.

The demand for cheese powder is expected to grow in the region owing to its widespread use as a key ingredient in snacks, ready meals, sauces, dips, dressings, and bakery products, among others. The presence of numerous fast food chains and the production of a wide variety of cheeses are expected to drive the growth of the North American cheese powder market.

The increased demand for convenience food products offers growth opportunities to cheese powder manufacturers. Moreover, there is a growing consumers interest in high-quality, artisanal, and specialty cheeses. Artisanal cheesemakers are gaining attention for their unique flavors, production methods, and localized offerings.

Major key players operating in the Cheese Powder are Land O'Lakes, Inc. (US), Kerry Group Plc (Ireland), Fonterra Co-operative Group Limited (New Zealand), ADM (US), Commercial Creamery Company (US).

Get 10% Free Customization on this Report:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=103908380