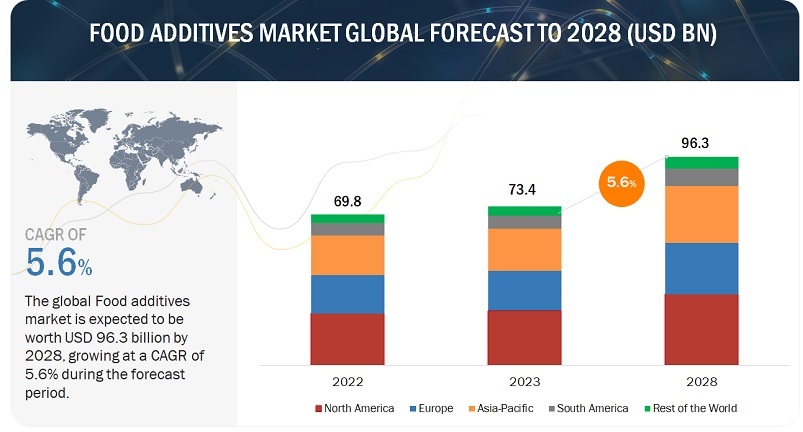

According to a research report "Food Additives Market by Type (Emulsifiers, Hydrocolloids, Preservatives, Dietary Fibers, Enzymes, Sweeteners, Flavors), Source (Natural, Synthetic), Form, Application (Food, Beverages), Functionality, and Region - Global Forecast to 2028" published by MarketsandMarkets, the food additives market is projected to reach USD 96.3 billion by 2028 from USD 73.4 billion by 2023, at a CAGR of 5.6% during the forecast period in terms of value. The food additives market is experiencing growth due to increasing consumer demand for natural and clean-label products, the expansion of the food and beverage industry, and technological advancements in food processing.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=270

The food additives market is expanding due to consumer demand for natural, healthy, and transparent products driving the market.

The burgeoning expansion of the food additives market is propelled by current trends emphasizing plant-based and natural ingredients, aligning with the surge in eco-conscious consumer preferences. A pronounced shift towards functional and health-focused foods is fostering demand for additives designed to impart nutritional benefits. Consumers now seek products that prioritize both taste and well-being, prompting innovations in additives for nutritional fortification. Furthermore, the increasing popularity of clean-label products has led to a heightened demand for additives that maintain transparency while enhancing overall product quality. Notably, technological advancements, particularly in encapsulation solutions, are gaining traction, contributing to improved stability for sensitive ingredients and reduced flavor loss. In response to evolving consumer priorities and sustainability considerations, the food additives market is witnessing robust growth, reflecting a dynamic industry poised for continued expansion.

The upswing in the Asia Pacific food additives market is fueled by surging demand for clean-label and natural additives. Consumers' increasing preference for transparent ingredient lists drives innovation in natural additives. Additionally, the flourishing food and beverage industry in rapidly urbanizing countries like China and India, coupled with a rising middle-class population, propels the market's growth. This trend reflects the region's dynamic shift towards processed and convenience foods, driving the need for advanced and sustainable food additives to meet evolving consumer preferences.

Make an Inquiry:

https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=270

In food additives, the surge in sugar substitutes is driven by health-conscious consumers and industry innovation.

The dominance of sugar substitutes in the food additives market is propelled by a dual influence of health-conscious consumer preferences and industry innovation. As consumers increasingly prioritize healthier lifestyles, the demand for sugar substitutes has surged, given their role in mitigating health concerns associated with excessive sugar consumption. Notably, the rising prevalence of conditions like diabetes and obesity has accelerated the adoption of sugar alternatives. This consumer shift aligns with the ongoing trend of clean-label products, where manufacturers are compelled to replace traditional sweeteners with healthier alternatives.

Key players, such as Cargill Incorporated (US), have strategically responded to this trend with innovative sugar substitute offerings. Cargill's introduction of C TruSweet and SweetPure in Europe reflects the industry's commitment to providing natural and clean-label sugar alternatives. These products cater to the demand for reduced-calorie options while maintaining the sweetness that consumers desire. The dominance of sugar substitutes is further accentuated by their versatility, enabling application across various food and beverage products without compromising taste, contributing to their overarching influence in the food additives market.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=270

North America dominated the food additives market during the study period.

The presence of key players such as Cargill, Incorporated (US), ADM (US), IFF (US), Ingredion Incorporated (US), Cp Kelco (US), Glanbia PLC (Ireland) and Darling Ingredients Inc. (US) underscores North America's dominance in the food additives market. These industry leaders strategically align with the region's dynamic trends, where the surge in demand for clean-label and plant-based products has become increasingly evident. North America's dominance in the food additives market is driven by the region's proactive response to the rising demand for clean-label and plant-based products. With consumers increasingly seeking healthier options, there's a notable surge in the adoption of natural additives and alternatives, such as plant-based stabilizers and preservatives. Major food manufacturers in North America are strategically reformulating their products to meet clean-label criteria, contributing to the region's prominence.

Additionally, the region is witnessing a significant shift toward functional foods and beverages, leading to the incorporation of specialized additives aimed at enhancing nutritional profiles. Consumer awareness of the impact of dietary choices on health is prompting the use of fortifying additives like vitamins and minerals.

Key players in this market include Cargill, Incorporated (US), BASF SE (Germany), ADM (US), IFF (US), Kerry Group PLC (Ireland), Ingredion Incorporated (US), Tate & Lyle (UK), Givaudan (Switzerland), Darling Ingredients Inc. (US), Chr. Hansen Holding A/S (Denmark), Novozymes (Denmark), Ashland (US), Cp Kelco (US), Glanbia PLC (US), and Sensient Technologies Corporation (US).