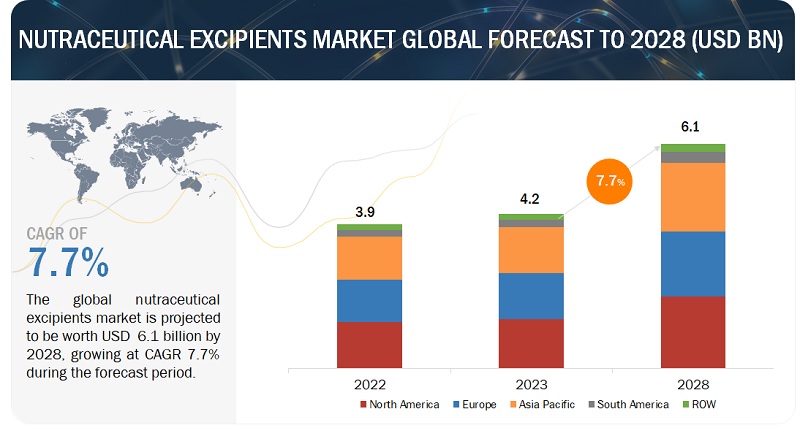

According to a research report "Nutraceutical Excipients Market by Product Source (Organic Chemicals, Inorganic Chemicals), Functionality (Binders, Colorants, Flavors & Sweeteners), End Product, Formulation, Functionality Application and Region - Global Forecast to 2028" published by MarketsandMarkets, the global nutraceutical excipients market will grow from USD 4.2 billion in 2023 to USD 6.1 billion by 2028, growing at a CAGR of 7.7% during the forecast period. The burgeoning popularity of nutraceuticals in recent years reflects their usage for diverse therapeutic purposes. This trend underscores their significance in addressing various ailments and diseases, ranging from cancer and heart conditions to cataracts, menopausal symptoms, insomnia, memory issues, gastrointestinal problems, headaches, and migraines caused by stress.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=247060367

The organic chemicals product source of the nutraceutical excipients segment is driving the market due to consumer preference for natural products, reduced allergenic potential, and a clean label trend.

The burgeoning nutraceutical excipients market is fueled by the escalating consumer demand for natural and organic ingredients. Consumers' heightened awareness regarding ingredient sourcing and quality in supplements and functional foods is a driving force behind this surge. This increasing consciousness directly influences the market's growth, as consumers actively seek excipients derived from organic materials to align with their preference for natural sources. Additionally, the potential allergenic risks associated with synthetic excipients further elevate the appeal of organic chemicals sourced from natural origins, particularly among sensitive consumer demographics seeking safer alternatives.

The dry formulation segment exhibits the highest CAGR, driving nutraceutical excipients market growth.

The increasing demand for dry excipients stems from their remarkable ability to offer formulation flexibility, allowing manufacturers to craft a wide array of dosage forms like tablets, capsules, powders, or granules. This versatility enables tailored formulations that cater to specific consumer preferences, optimizing drug delivery systems accordingly. Additionally, the compatibility of dry excipients with a diverse range of active ingredients makes them highly sought-after across pharmaceuticals, nutraceuticals, and various industries, providing manufacturers with extensive application possibilities.

Make an inquiry:

https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=247060367

North America accounts for the largest share of the nutraceutical excipients market and is witnessing growth due to the strong presence of key companies and increasing lifestyle diseases & health concerns.

In North America, numerous prominent players and leading manufacturers dominate the nutraceutical industry. These influential companies play a pivotal role by consistently engaging in research, innovation, and the development of new products, significantly contributing to the market's growth. The region's escalating health concerns, encompassing issues like obesity, cardiovascular diseases, and lifestyle-related conditions, have prompted consumers to actively pursue preventive healthcare measures. As a result, there's a heightened demand for nutraceutical products perceived as valuable in addressing these health issues. This increased demand directly fuels the market for nutraceutical excipients, essential components in the formulation of these sought-after health-focused products.

The key players in the nutraceutical excipients market include International Flavors & Fragrances Inc (US), Kerry Group plc (Ireland), Ingredion (US), Sensient Technologies Corporation (US), Associated British Foods plc (UK), BASF SE (Germany), Roquette Frères (France), MEGGLE GmbH & Co. KG (Germany), Cargill, Incorporated (US), Ashland (US), IMCD (Netherlands), Hilmar Cheese Company, Inc (US), Air Liquide (France), Azelis Group (Luxembourg), and Biogrund GmbH (Germany).