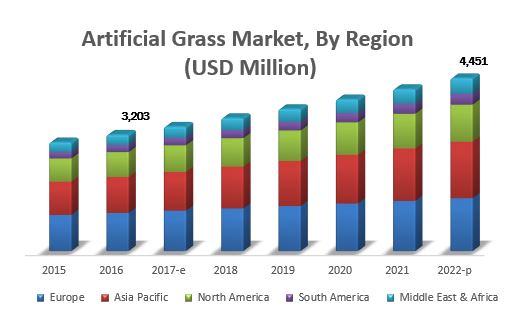

The report "Artificial Grass Market by Installation (Flooring, Wall Cladding), Fiber Base Material (Polyethylene, Polypropylene, Nylon), Application (Contact Sports, Non-contact Sports, Leisure, Landscaping), Infill Material, and Region - Global Forecast to 2022", The artificial grass market is estimated to be valued at USD 3.20 Billion in 2017 and is projected to reach USD 4.45 Billion by 2022, at a CAGR of 6.8% during the forecast period. The market is driven by factors such as increased applications in the landscaping space, replacement of natural grass with artificial grass in sports fields, and growing popularity of various sports in different regions.

Objectives of the study are as follows:

- To define, segment, and project the global market size with respect to application, installation, fiber base material, infill material, and key regions

- To provide detailed information about the major factors influencing the growth of the market (drivers, restraints, opportunities, and industry-specific challenges)

- To analyze the opportunities in the market for stakeholders and provide the competitive landscape of the market leaders

- To project the size of the market and its submarkets, in terms of value and volume, with respect to the regions (along with the key countries)

- To strategically profile the key players and comprehensively analyze their market position and core competencies

- To analyze the competitive developments such as expansions & investments, mergers & acquisitions, and new product developments in the artificial grass market

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238480246

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=238480246

Based on installation, the market has been segmented into flooring and wall cladding. The flooring segment dominated the market in terms of both value and volume in 2016. Rising popularity and acceptance of synthetic sports fields for indoor as well as outdoor sports, along with extended applications in landscaping are the key factors that drive the flooring segment in the artificial grass market. In developed countries, the backing of advanced technologies with regard to product development and sports infrastructure development has fueled the demand for artificial grass.

Based on fiber base material, the market has been segmented into polyethylene, polypropylene, and nylon. The polyethylene segment is estimated to account for the largest share of the market in 2017. It is widely preferred by various artificial grass manufacturers due to due to its durability, softness, and resiliency, which is required for technically demanding contact sports pitches.

Based on application, the artificial grass market has been segmented into contact sports, non-contact sports, landscaping, and leisure. The contact sports segment is estimated to be the largest segment in 2017 and this trend is expected to continue through the forecast period owing to factors such as the increase in number of football pitches across the world, increase in investments in hockey in countries such as India, and growth in popularity of American football in the US.

In 2017, Europe is estimated to account for the largest share of the artificial grass market. Factors such as the presence of leading artificial grass manufacturers that operate on a global scale such as Tarkett (France), SportGroup (Germany), Victoria PLC (UK), and SIS Pitches (UK) have boosted the demand for artificial grass in the European market. Furthermore, advanced technologies and supporting infrastructure for promoting sports, especially football, also fuels the artificial grass market growth in this region.

Request for Customization:

This report includes a study of the marketing and development strategies, along with the product portfolios of the leading companies. It includes the profiles of leading companies such as DowDuPont (US), Tarkett (France), Controlled Products (US), Shaw Industries Group (US), and Victoria PLC (UK). Other players include Act Global (US), SportGroup (Germany), TigerTurf (New Zealand), SIS Pitches (UK), Matrix Turf (US), Nurteks Hali (Turkey), Soccer Grass (Brazil), Limonta (Italy), Sportlink (Brazil), and El Espartano (Argentina).

Target Audience:

- Artificial grass manufacturers and equipment suppliers

- Artificial grass traders, distributors, importers, exporters, and suppliers

- Yarn manufacturers

- Commercial research & development (R&D) organizations, turf recycling organizations, and financial institutions

- Artificial grass installers, infill solution providers, architects, sports field engineers, and polymer manufacturers