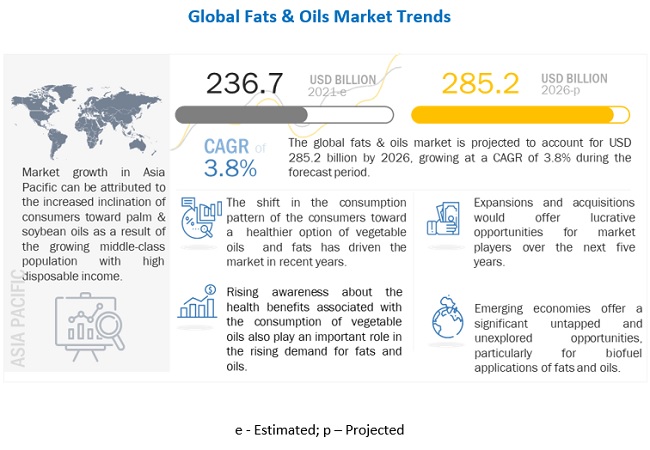

According to MarketsandMarkets the global fats and oils market is estimated at USD 236.7 billion in 2021; it is projected to grow at a CAGR of 3.8% to reach USD 285.2 billion by 2026. The market has a promising growth potential due to a plethora of factors, including the rising awareness to use healthier alternatives such vegetable-derived oils among the consumers, increasing health concerns about traditional fats, and increased consumption of processed and baked food items.

Apart from food industry, vegetable fats and oils are also increasingly used for industrial applications, such as soaps, detergents, paints, oleochemicals, the major one of them being biodiesel.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

COVID-19 Impact on the Fats & Oils Market

The supply and demand for fats & oils in the global market has shifted due to the coronavirus crisis, with an increasing uncertainty related to prices. Palm oil, which is the largest type of oil produced globally, faced the impact as demand dropped across the world, trade was disrupted, and production got hampered in Indonesia and Malaysia, according to the top vegetable oils producers, such as Wilmar International and Mehwah Group, which operate in the region. Efforts were being made in many countries to maintain stability in the market. According to the Indonesian Palm Oil Producers Association (GAPKI), exports to China plunged by 57% in January 2019-2020. Governments from countries such as India, China, and the US made exemptions for the sector to continue their businesses with minimal capacity amid the lockdowns. As the production continued, these companies could mitigate the considerable impact by the continuity of operations.

Opportunity: Emerging application of fats and oils as substitutes of trans-fats

Trans-fats are unsaturated fatty acids formed during the hydrogenation of vegetable oils or are found in animal products naturally produced in the gut of grazing animals. Consumption of trans-fat raises the level of low-density lipoprotein cholesterol in the blood. An elevated LDL blood cholesterol level can increase the risk of developing cardiovascular. Trans-fats are found in many food products, such as vegetable shortenings, stick margarine, refrigerated dough products (such as biscuits and cinnamon rolls), snack foods, coffee creamers, cookies, cakes, frozen pies, frozen pizza, and fast food.

Owing to the increased health consciousness among consumers, trans-fats are gradually replaced by a much healthier substitute, namely unsaturated liquid vegetable oils, such as olive, canola, corn, or soy oils.

On the basis of source, vegetable segment is expected to retain its dominance in the foreseeable period

Vegetable oils from sunflower, rapeseed, soybean, palm, cottonseed, and coconut are highly used in food applications which has driven the market for vegetable-sourced oils. The qualities associated with vegetable oils such as low-fat, low-cholesterol, and low-calories content are registering growth in the segment. Also, the variety of use of vegetable oils in food as well as other industries such as pleo-chemical industries, animal feed, and energy & biomass industry has also driven the market for vegetable oils.

On the basis of form, liquid oils are projected to witness the highest growth in the market

The liquid form of fats & oils is forecasted to dominate the market. However, the physical characteristics of fats and oils depends upon a lot of factors such as degree of unsaturation, the length of the parent carbon chain, the isomeric forms of the fatty acids, molecular configuration, and processing variables, but it is believed that the liquid oils are more unsaturated and are hence more preferred by the consumers.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=6198812

Asia Pacific is projected to be the fastest-growing region in the fats & oils market.

The Asia Pacific region is projected to be the fastest-growing market for fats & oils. The region is home to two important palm and palm kernel oil-producing countries namely Malaysia, and Indonesia: and two major fats & oils consuming countries namely China, and India. This is one of the significant factor which ensures that Asia pacific region is the largest as well as the fastest-growing market in fats & oils.

Key Market Players:

Key global market players offer wide range of fats & oils products in the retail chain. While prominent palm oil producing companies are present in Asia pacific region. The soybean oil producing companies capture the North American market. The key companies in the fats and oils market are Associated British Foods PLC (UK), Archer Daniels Midland Company (US), Bunge Limited (US), Wilmar International Limited (Singapore). Various strategies, such as expansions, mergers & acquisitions, and new product launches, were adopted by the key companies to remain competitive in the fats & oils market.