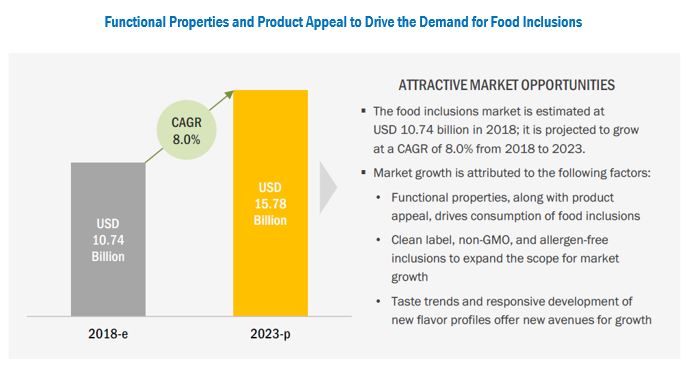

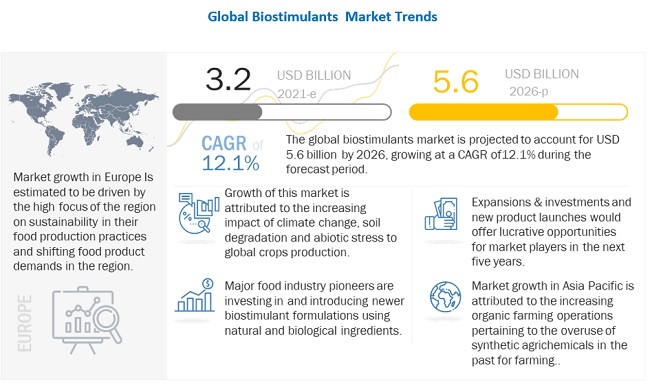

The report "Biostimulants Market by Active Ingredients (Humic Substances, Seaweed Extracts, Microbial Amendments, Amino Acids), Mode of Application (Folier, Soil Treatment, Seed Treatment), Form (Liquid, and Dry), Crop Type, & by Region - Global Forecast to 2026", The Biostimulants Market was valued at USD 3.2 billion in 2021; it is projected to grow at a CAGR of 12.1% to reach USD 5.6 billion by 2026.

Biostimulants encompass a diverse range of active ingredients, which include microbial inoculants, amino acids, humic acids, fulvic acids, seaweed extracts, and others (which include polysaccharides, trace minerals, and vitamins). These active ingredients are considered complementary to crop nutrition and crop protection products, and hence, there is a growing need for biostimulants from growers across the world. Furthermore, there is an increased demand for sustainably produced food, with a lesser concentration of synthetic chemicals and a higher concentration of biologicals. Hence, biostimulants are helping to address this issue sustainably by providing protection against stress and stimulating the plants growth.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1081

The Amino Acid by Active ingredient is projected to achieve the fastest growth in the Biostimulants Market.

Amino acids are available in the agricultural market as active ingredients that can cause an impact on the biochemical and physiological processes and functions of plants. They can be used as foliar sprays to increase yield, improve quality, enhance stress resistance, and facilitate the early maturity of crops. Enriching crop plants in essential amino acids have been observed to be of both economical and humanitarian interest.

The Liquid Form segment is estimated to account for the largest market share in the Biostimulants Market.

Liquid formulations provide various options to crop growers to mix the biostimulants with pesticides, fertilizers, or adjuvants. Some biostimulant active ingredients dissolve readily in a liquid solvent, such as water or a petroleum-based solvent. When mixed with the solvent, they form a solution that will not settle out or separate. Formulations of these biostimulants usually contain the active ingredient, the solvent, and one or more other ingredients.

The Fruits and Vegetables segment by crop type is estimated to account for the largest market share of the Biostimulants Market over the forecast period.

Biostimulants have played a vital role in fruits and vegetables to enhance the crop size, quality, health, stress tolerance, and reduce residue levels. The application of biostimulants in fruits has led to better fruit development; high crop yield; better quality with respect to size, color, and sugar content; prevention of fruit drops; and enhanced ripening.

The Foliar Method of Application is estimated to see the fastest market growth in the Biostimulants Market during the forecast period.

Foliar spray application of biostimulants is one of the most widely used methods that help in maximizing the productivity of plants. Plants absorb nutrients through the roots and the foliage. Many plant nutrients are needed in such great quantities that it is impractical to supply them through the foliage. However, when soil conditions are unfavorable, it may be desirable to make foliar applications of the biostimulants. When biostimulants are applied to the plants foliage, smaller quantities of the fertilizer or other agrochemical material are needed than when applied to the soil. The danger of fixation and/or leaching is also reduced when it is applied to the foliage of the plant.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=1081

Asia Pacific is estimated to be the largest market.

The agriculture industry in Asia, particularly in the Southeast Asian countries, has witnessed effective transformation due to various technological advancements. This has resulted in the adoption of intensive agricultural practices and has led to a decrease in the nutrient levels of the soil. To revitalize the soil, the use of inoculants and biostimulants has been recommended by the agricultural authorities in various countries of Asia. Biostimulants enhance the physiological activities of the seed for early emergence and for optimum crop development at later stages under various climatic and agronomic conditions in the region.

Key Market Players:

The key players in this market include BASF SE (Germany), UPL (India), Valagro S.p.A (Italy), Gowan Group (US), FMC Corporation (US), ILSA S.p.A (Italy), Rallis India Limited (India), Haifa Group (Israel), Adama Ltd. (Israel), Biovert-Manvert (Spain), Koppert Biological Systems (Netherlands), Rovensa (Spain), and AgriTecno (Spain). These players in this market are focusing on increasing their presence through agreements and collaborations. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.