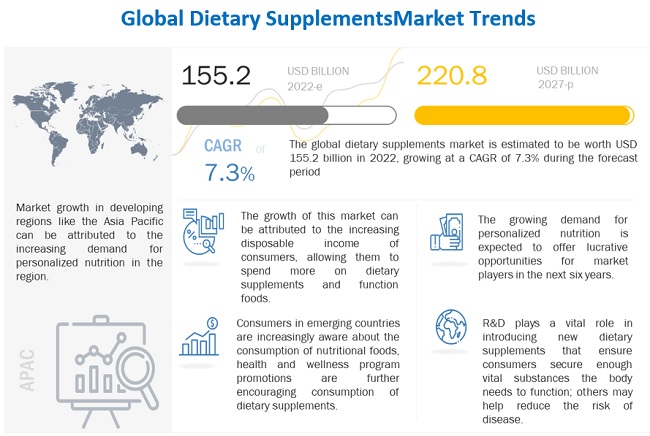

According to MarketsandMarkets, the Dietary Supplements Market is estimated at USD 155.2 billion in 2022; it is projected to grow at a CAGR of 7.3% to reach USD 220.8 billion by 2027.

The impact of COVID-19 will further shift the demand towards dietary and nutritional supplements. Food supplements are likely to experience high growth due to the ongoing pandemic. The impact of COVID-19 and the severity of the coronavirus has highlighted the importance of immunity. The link between immune function and nutrition is further projected to drive the adoption of dietary supplements.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=973

The vitamin segment is projected to be the fastest-growing throughout the forecast period. Vitamins differ from other biologically important molecules like proteins, carbohydrates, and lipids in various ways. Although the latter substances are also required for proper body functions, animals can synthesize almost all of them in adequate quantities. Vitamins, on the other hand, cannot be synthesized in sufficient amounts to meet body requirements and must therefore be obtained through the diet or from a synthetic source. For this reason, vitamins are referred to as essential nutrients.

The rising number of health-conscious consumers has triggered the demand for additional dietary supplements. In the pharmaceutical industry, some dietary supplements play an important role in the treatment of several diseases. Athletes and sports personnel view dietary supplements as performance-enhancing products. Hence during the forecast period, these additional segments are expected to witness a faster growth rate in terms of value sales.

Tablet is the most preferred mode of application of Dietary Supplements as they provide long lasting benefits. Tablets are widely used and offer convenience, affordability, a wide range of dosing patterns, simple packaging, storage, and cost effectiveness. Tablets also have a longer shelf life than other types of dietary supplements, making them more popular. Their compressibility ensures that they can hold more nutrients than a capsule while being compact. Tablets can be crushed and mixed into a drink for those who cannot swallow pills

Rising instances of vitamin deficiency and growing awareness about the health benefits of dietary supplements will drive the overall growth of the adults segment. The top three most common dietary supplements used by adults were multivitamin-mineral, vitamin D, and omega-3 fatty acids. Government programs, such as the Supplemental Nutrition Assistance Program (SNAP) or the Food Distribution Program on Indian Reservations (FDPIR), serve as a resource for low-income adults by supplementing food budgets to support healthy lifestyles.

Make an Inquiry @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=973

North America accounted for the largest share of the dietary supplements market during the forecast period. The large share of North America can be attributed to the rising prevalence of chronic diseases and the increasing awareness among consumers regarding the health benefits of dietary supplements. The market for dietary supplements in North America is moving toward maturity, due to which it has witnessed steady growth. The market is favorable for innovative and new ingredients of better and enhanced quality.