The global

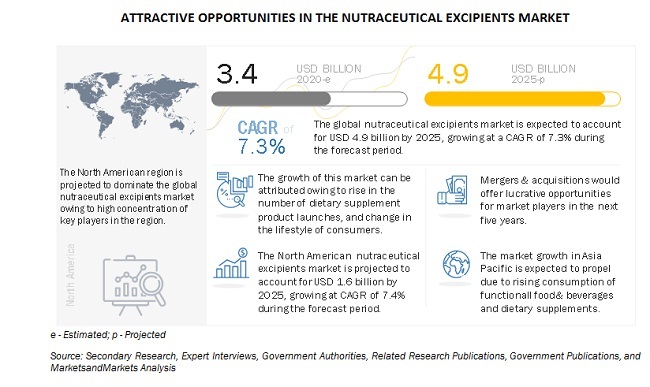

nutraceutical excipients market size is estimated to account for nearly USD 3.4 billion in 2020 and projected to grow at a CAGR of 7.3%, to reach nearly USD 4.9 billion by 2025. The market for nutraceutical excipients is been witnessing rise in demand, owing to the increase in consumption of nutraceutical in the global market. Consumers in the global market are increasingly preferring dietary supplements and fortified food & beverage products as a part of their daily dietary lifestyles. This gives immense opportunities for growth of nutraceutical excipients, which are largely used binding, coating, filling, coloring, flavoring, disintegrating, and lubricating agent. It is an inactive ingredient that is added along with the active nutraceutical ingredients in the product formulation. Furthermore, developed countries such as the US is already witnessing an upshift in the demand, however, the growth potential for nutraceutical excipients is growing at an exponentially high rate in the Asia Pacific and European countries.

Nutraceutical excipients are non-active nutraceutical ingredients that are included in the production of nutraceutical formulations. Excipients are also used to enhance the therapeutic effects of active ingredients in the final dose. Nutraceutical active ingredients are biologically functional molecules or components, which affect the nutritional uptake, balance, and health of a human body, and that mostly aims to supplement the nutritional profile provided by staple foods. Moreover, excipients are essential for the timely and precise delivery of nutraceutical components. In addition, maintaining optimum levels of active ingredients in the nutraceutical products, such as vitamins and minerals, is a key function of excipients.

The key players in this market include DuPont (US), BASF SE (Germany), Kerry Group PLC (Ireland), Ingredion Plc (US), Sensient Technologies (US), Associated British Foods (UK), Roquette Freres (France), Meggle Group Wasser (Germany), Cargill Inc (US), Ashland Global Holdings Inc (US), Seppic (France), Shin-Etsu Chemical Co Ltd (Japan), Fuji Chemical Industries Co Ltd (Japan), Pharmatrans Sanaq AG (Switzerland), Pioma Chemicals (India), Gattefosse (India), W.R.Grace & Co (US), Omya (Switzerland), Grain Processing Corp (US), and Gangwal Chemicals Pvt Ltd (India). The key market players, along with the other players, adopted various business strategies such as new product launches, expansions, and joint ventures & agreements, in the last few years, to meet the growing demand for nutraceutical excipients.

Major players in the market are mainly focusing on undertaking expansions for developing research centers to meet the growing requirements of the end-industry manufacturers by formulating innovative products/solutions. The core strengths of the key players identified in this market are growth strategies such as expansions & investments and mergers & acquisitions. The undertaking of mergers & acquisitions as a key growth strategy has enabled the market players to enhance their presence in the nutraceutical excipient market. The key players, such as DuPont (US), Ingredion Plc (US), Roquette Freres (France), and few others have undertaken these strategies to improve their distribution network, gain a stronger foothold, and enhance market share. For example, DuPont inaugurated a new facility in Oegstgeest, the Netherlands. This development will benefit the company in expanding its research capabilities for its nutrition and bioscience segment along with specifically strengthening its position in Europe, the Middle East, and Africa regions.

Cargill Incorporated (US), is involved in the manufacturing and marketing of food ingredients, agricultural products, risk management & financial services, and industrial products around the globe. The company’s key business segments include animal nutrition, food & beverage, bio-industrial, food service, agriculture, risk management, meat & poultry, industrial, beauty, pharmaceutical, and transportation. It offers a wide range of excipient products under its pharmaceutical segment to several players in the pharmaceutical and nutraceutical industry.

Associated British Foods (ABF) Plc (UK), was formerly known as Food Investments Ltd until 1982. It is a leading manufacturer and processor of food & ingredients and is also involved in retail businesses of its food & ingredients. The company operates a majority of its business through five major segments, such as sugar, agriculture, retail, grocery, and ingredients.

ABITEC, an ABF ingredients company, is the major provider of excipients products, which include lubricants, binders, coating agents, and flavoring agents to various players in the pharmaceutical and nutraceutical industries. In addition, ABF commercializes a range of other excipient products through its other brand, SPI Pharma (US), a manufacturer of pharmaceutical and nutraceutical products, which offers a line of functional excipient products, catering to the demand of key players in the pharmaceutical and nutraceutical industries. SPI Pharma operates under the Associated British Foods (ABF) Plc ingredients division, ABF Ingredients (UK). Of its subsidiaries, ABF Ingredients (UK) has a global presence in nine countries, which include the US, Brazil, Germany, France, the UK, Finland, India, Singapore, and China, and has nearly five companies operating under it.

Kerry Group Plc (Ireland), is a leading global manufacturer of food ingredient products and flavors and a supplier of value-added brands. At first, it operated as a dairy cooperative in Ireland, and in the later phase, as manufacturers of real and wholesome ingredients. It provides a broad range of excipients under its product line of pharmaceutical products through its taste & nutrition business segment.

North America accounted for the largest market share in 2019. The nutraceutical excipients market in North America is dominating, owing to the concentration of the global players such as DuPont (US), Kerry (Ireland), Cargill (US), and Ingredion (US). The market for nutraceutical excipients here is mature, and hence, the growth is moderate compared to other regions. Other factors contributing to the growth of nutraceutical excipients in North American region include the busy lifestyle of consumers, prevalence of chronic diseases due to hectic lifestyles, and an increase in awareness among consumers regarding the health benefits of nutritional foods, including food supplements, which has driven the demand for functional food products. In addition, the use of technological advancements and new product launches have made excipients available for a wide range of applications in the fortified food & beverage, dietary supplements, and nutraceuticals sectors, which is projected to drive the growth of the market in the region.