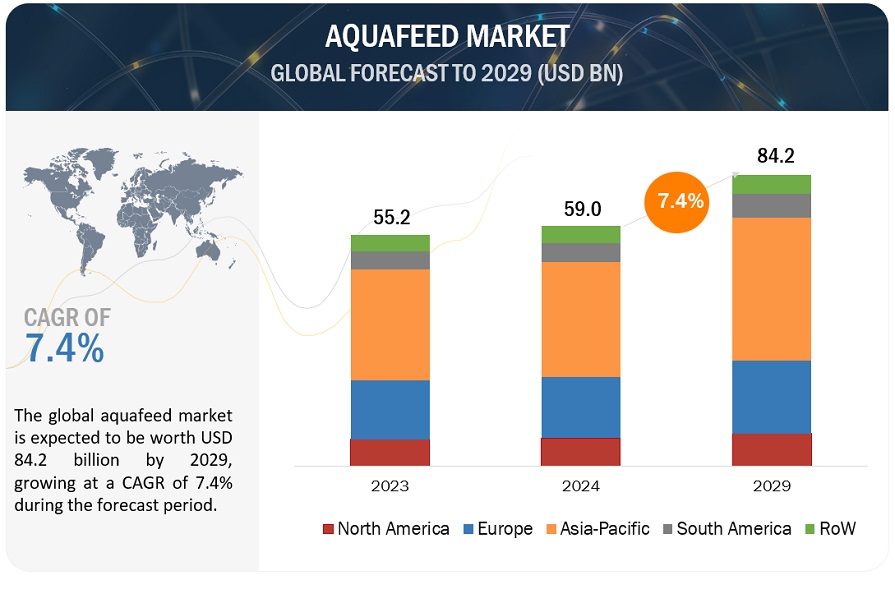

The global aquafeed market is projected to reach USD 88.0 billion by 2028, at a CAGR of 7.3% over the forecast period. It is estimated to be valued USD 61.8 billion in 2023. Several important factors are driving up demand for aquafeed products on a global scale. First, a growing worldwide population has an increased need for seafood, and aquaculture offers a sustainable way to meet this demand. Fish and prawn farming has become more popular because of the depletion of wild fish stocks. Aquafeed is crucial for the healthy growth and development of aquaculture aquatic species, increasing their output and decreasing their reliance on foraging wild fish. Aquafeed products are in high demand to support the expansion of the business since advances in aquaculture technology and practises have made it more effective and financially viable.

Some of the Prominent Key Players are:

- ADM (US)

- Cargill, Incorpoarted (US)

- Ridley Corporation Limited (Australia)

- Nutreco (Netherlands)

- Alltech (US)

- Purina Animal Nutrition (US)

- Adisseo (Belgium)

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1151

By ingredients, soybean segment is projected to have the largest share during the forecast period.

Soybeans are among the non-fish sources of omega-3 fatty acids, proteins, and unsaturated fats. Soy protein is fed to farm-reared fish and shellfish to enhance their overall growth and development. Some of the commonly used soybean products in aquafeed include heat-processed full-fat soybean, mechanically extracted soybean cake, solvent-extracted soybean meal, and dehulled solvent-extracted soybean meal. Soybean isolates and different varieties of genetically modified soybeans are being introduced to replace fishmeal, which is a rich source of amino acids.

By species, fish segment is projected to have fastest growing rate during the forecast period.

In the aquafeed market, the fish segment is expanding for a variety of reasons. The need for high-quality and nutritionally balanced aquafeed is being driven by the increasing demand for fish protein on a global scale, the depletion of wild fish supplies, and the growth of aquaculture. To ensure optimum development, health, and sustainability in the sector, fish farming, with its well-established practises and different species, needs specialised feeds.

Make an Inquiry:

https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=1151

Asia Pacific is expected to have the fastest growing rate during the forecast period.

The aquafeed market is expanding in the Asia Pacific region because of reasons like a growing population, rising seafood demand, favourable environmental conditions for aquaculture, technical improvements, and government backing. The expansion of the aquaculture sector is being fuelled by economic growth, shifting dietary tastes, and the need for sustainable protein sources, which is causing a commensurate rise in demand for aquafeed products.