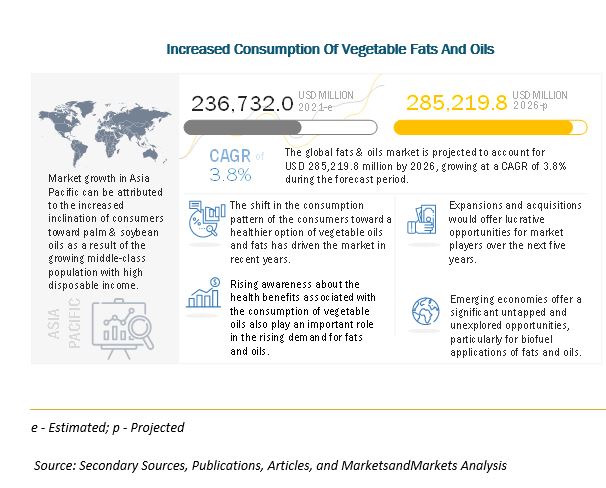

The fats and oils market is estimated to be USD 236.7 billion in 2021; it is projected to grow at a CAGR of 3.8% to reach USD 285.2 billion by 2026. The global fats & oils market is being highly driven by robust demand dynamics emanating from both the food and non-food application sectors. Although country-level dietary guidelines advocate a switch to unsaturated fats, the sales of butter and all the other vegetable oils are witnessing decent growth because they are perceived as being more natural. The fats & oils market is also driven by non-food utilization, particularly for the production of oleochemicals and biofuels. Mandatory blending targets for biofuels have encouraged the uptake of these commercially important lipid compounds in Western markets, which were soon adopted by developing countries.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6198812

The fats and oils market has been growing steadily in developed countries and emerging countries, such as the US, Brazil, China, India, and Indonesia. Among vegetable oils, palm oil remained the most popular with around 30% of the market share. Animal fats find major applications in pet food, animal feed, and other industrial purposes such as biodiesel and oleochemicals. Oils of plant origin have been predominantly used for food-based applications. The fats & oils market, by form, is estimated to be dominated by the liquid segment in 2021.

On the basis of type, the vegetable oil is projected to be the largest segment during the forecast period.

The health benefits, easy availability, and cost-effectiveness are some of the factors that has driven the market for fats & oils. Within vegetable oils, the palm oil segment has dominated the market, as it is easily available and is relatively more stable than other oils.

On the basis of source, vegetable segment is expected to retain its dominance in the foreseeable period.

Vegetable oils from sunflower, rapeseed, soybean, palm, cottonseed, and coconut are highly used in food applications, which has driven the market for vegetable-sourced oils. The qualities associated with vegetable oils, such as low-fat, low-cholesterol, and low-calories content, are registering growth in the segment. Also, the variety of uses of vegetable oils in food as well as other industries such as pleo-chemical industries, animal feed, and the energy & biomass industries has also driven the market for vegetable oils.

Request for Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=6198812

Asia Pacific is projected to be the fastest-growing region in the fats and oils market.

The Asia-Pacific region is projected to be the fastest-growing market for fats & oils. The region is home to two important palm and palm kernel oil-producing countries, namely Malaysia and Indonesia, and two major fats and oil-consuming countries, namely China and India. This is one of the significant factors that ensures that the Asia-Pacific region is the largest as well as the fastest-growing market in fats & oils.

Key Market Players:

Key global market players offer wide range of fats & oils products in the retail chain. While prominent palm oil producing companies are present in Asia pacific region. The soybean oil producing companies capture the North American market. The key companies in the fats and oils market are Associated British Foods PLC (UK), Archer Daniels Midland Company (US), Bunge Limited (US), Wilmar International Limited (Singapore). Various strategies, such as expansions, mergers & acquisitions, and new product launches, were adopted by the key companies to remain competitive in the fats and oils market.