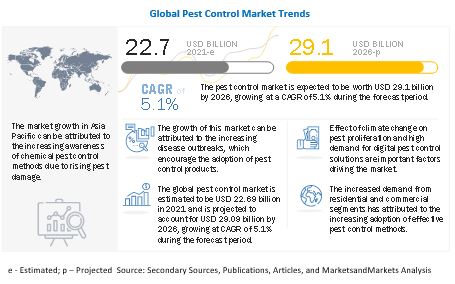

The report "Pest Control Market by Pest Type (Insects, Rodents, Termites), Control Method (Chemical, Mechanical, Biological), Mode of Application (Sprays, Traps, Baits), Application (Residential, Commercial, Industrial), and Region – Global Forecast to 2026" estimated at USD 22.7 billion in 2021; it is projected to grow at a CAGR of 5.1% to reach USD 29.1 billion by 2026.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=144665518

Pest control has witnessed strong growth due to public health concerns and an increase in the frequency of pest infestations due to climate changes. In countries such as the US, strong regulatory requirements concerning pest control and environmental protection laws have helped bolster the market demand and attract service providers to set up business units. With the rise in demand and preference for a clean and pest-free environment, pest control manufacturers and service providers have been strategizing on coming up with innovative solutions for the market at a reasonable price. The surge in global Internet penetration would be another influential trend in driving the market in terms of value sales. Manufacturers and distributors make the best of the Internet in spreading awareness about their products and services among target consumers and simultaneously generating revenue sales.

Insects sub-segment in by pest type segment is estimated to account for

the largest share in the pest control market.

There are more than a million described species of insects, with 90% of all animal forms on earth consisting of insects. Insects such as mosquitoes, ants, cockroaches, and tiny moths destroy household materials and may cause ill-effects on the human body. Of the different types of insects, certain species are classified as pests and are controlled using chemicals, biologicals, and other mechanical means. The use of chemicals is the mainstream method to reduce losses caused by insect pests. Thus they are estimated to dominate the by pest type segment.

In by control method segment, the software and services sub-segment is

projected to account for the fastest market growth in the pest control market.

The software & services segment plays an integral part in digital pest control solutions while implementing platforms and executing activities related to them. These services include consulting, integration, and support and maintenance, which are required to deploy, execute, and maintain pest control. AI and IoT are trending technologies that help improve smart pest monitoring and control. According to one of the primaries conducted in Bayer CropScience, India, “The use of advanced information technologies and connected traps are among the new solutions offered by companies such as the Bayer Rodent Monitoring System.

Sprays sub-segment by mode of application is projected to account for

the largest market share of the pest control market over the forecast period.

Spray-based pest control solutions incorporate a liquid formulation which is deployed either in an aerosol form, or a pressurized spray container. The spraying requirements may differ based on the pest type, climate conditions in the region, and the type of chemical used. Spray formulations are used to control a wide array of pests, including flies, cockroaches, ants, scorpions, silverfish, spiders, bed bugs, and ticks. Residual sprays are considered effective as the pesticides are mixed with adjuvants such as surfactants, which allow the pesticide to remain in contact with the infested area or insect body for a limited time.

Industrial sub-segment by application is projected to account for the

fastest market growth in the pest control market over the forecast period.

Pest control in factories and manufacturing units is mandatory in the US. The mandate may differ on a case-by-case basis. For instance, pest control requirements in pharmaceutical and food manufacturing units are stringent to prevent any type of contamination in the product. In industrial facilities, factories, and manufacturing plants, certain birds cause serious problems as they may get caught in the machinery or dig holes in the roofs. The rapid urbanization globally is driving the market growth of the segment.

Speak to Analyst @ https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=144665518

North America is estimated to dominate the global pest control market

over the forecast period.

According to reports by major service providers, Rentokil Initial Plc (UK) and Anticimex (Sweden), North America occupies nearly 50% of the global pest control market. This is attributed to the increase in the number of services available in the US and a high rate of urbanization in the US and Canada. The strengthening of the housing market and a steadily improving economy have led to increased investments in both residential and commercial properties. These factors are driving the market in the region.

The key players in this market include Bayer AG, Corteva Agriscience, BASF, Sumitomo Chemical Co., FMC Corporation, Syngenta AG, ADAMA, and Bell Laboratories. These players in this market are focusing on increasing their presence through agreements and collaborations. These companies have a strong presence in North America, Asia Pacific and Europe. They also have manufacturing facilities along with strong distribution networks across these regions.