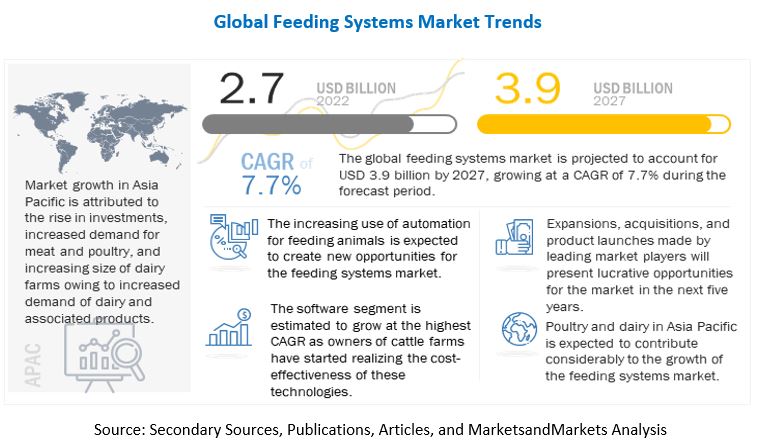

The global feeding systems market is projected to reach USD 3.9 billion, by 2027, at a CAGR of 7.7% from 2022 to 2027. The growing size of dairy farms, increasing focus of major companies on technological advancements as well as product launches and developments, and substantial cost savings associated with automated feeding systems are the major driving factors for the market. The market also faces some challenges like high capital requirements at the initial stage of installation, which may discourage small and medium-sized farms from automating the feeding process.

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=102235948

DeLaval is a market leader providing integrated milking solutions designed to improve dairy farmers’ production, animal welfare, and overall quality of life. The company develops and manufactures equipment for milk production and animal husbandry, including feeding systems worldwide. DeLaval offers highly efficient system solutions for milking, farm and herd management, animal traffic control, feeding, cooling, manure handling, ventilation, and energy recovery. The company supplies highly efficient solutions for cattle feeding, which help in reducing costs and increasing productivity. It has a strong global presence, spanning Europe, the Middle East, Africa, the Americas, and the Asia Pacific. In November 2018, DeLaval (Sweden) announced a partnership with CEJA (European Council of Young Farmers Home) to help farmers in the European Union for better sustainability in the long-term process of farming.

Trioliet B.V provides various solutions mainly to cattle farming. The solutions offered by the company include feeders, weighing systems, and loading equipment. The various feeders devised by the company for feeding bovine animals include mixer feeder wagons and self-loading mixer feeders. The company also provides feeding solutions to dairy farms worldwide. It has a presence in over 50 countries. In 2020, the company launched Triotrac M. It is self-propelled machine and has one vertical auger and a cutting-loading system with a loading rotor to load the feed into the mixing tub. The unique loading system ensures that the feed is processed cleanly and without any wastage during the loading process.

Get 10% Free Customization on this Report:

https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=102235948

Lely provides automated feeding, forage harvesting, and milking robot solutions for the agricultural sector. It also offers milking solutions such as robotic milking systems, used milking robots, and detection systems. The company’s product portfolio comprises feeding solutions such as feed pushers, individual feeders, calf feeders, selection boxes, animal feeding solutions, and housing solutions (including lighting systems, mobile barn cleaners, hygienic housing products, and cubicle solutions). Lely sells its products through dealers in Canada, Ireland, Australia, New Zealand, the UK, the US, Spain, Italy, Norway, Portugal, Sweden, Japan, Israel, Estonia, Czech Republic, South Korea, Slovakia, Iceland, and Cyprus. The company is widening its product portfolio and launched Lely Exos in October 2020, first concept for the fully autonomous harvesting and feeding of fresh grass.

The importance of feeding systems is increasing in the region due to the increasing demand for performance-boosting feed for cattle and animal welfare. There has been an increasing shift from conventional to automated systems in the region over the last 30 years due to technological advancements and the high affordability of animal rearers in the region. North American farm owners are focusing on catering to the growing demand from consumers for dairy and meat products. This has led various companies in the global market to develop innovative feeding systems such as individual feeders and group feeders.

In North America, the demand for feeding systems has picked up rapid pace, particularly in the US. Seeing this demand, Lely (Netherlands) introduced Lely Park, its new commercial hub and complex, launched in June 2022. With this development, Lely will be able to greatly boost its production capacity to fulfill the rising needs of North American farmers.

Request Sample Pages:

https://www.marketsandmarkets.com/requestsampleNew.asp?id=102235948