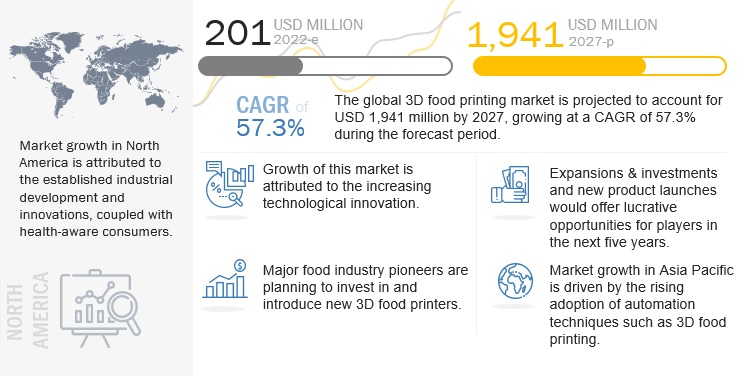

According to a research report "3D Food Printing Market by Vertical (Government, Commercial, and Residential), Technique (Extrusion based printing, Selective laser sintering, Binder jetting and Inkjet printing), Ingredient and Geography - Global Forecast to 2027" published by MarketsandMarkets, the 3D food printing market is estimated to account for nearly USD 201 million in 2022 and is projected to reach a value of nearly USD 1,941 million by 2027, growing at a CAGR of 57.3% from 2022. Large-scale manufacturing of food in commercial kitchens has exacerbated the problem of food waste. 3D food printing is a distinguished approach to reducing waste throughout consumption by utilizing food products such as meat off-cuts, leftover fruits and vegetables, and seafood by-products. Thus, with increasing awareness among consumers about food wastage and environmental issues, more consumers and food suppliers are anticipated to adopt 3D food printers. This is projected to drive the 3D food printing market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=267692011

By ingredient type, the carbohydrate segment is estimated to account

for the largest share in the 3D food printing market in 2022.

On the basis of ingredient type, the carbohydrate segment is estimated to dominate the 3D food printing market in 2022. Carbohydrate is the most widely used ingredient type used in 3D food printing because of the gelatinization property of carbohydrates. Increasing demand of carbohydrate-based food such as bakery products, confectionaries, driving the demand of carbohydrate type.

By vertical, commercial segment is projected to be the fastest-growing

segment during the forecast period in the 3D food printing market

During the forecast period, the commercial segment is projected to grow at the highest CAGR in the bakery processing equipment market, in terms of value. Most of the companies working toward the development of the 3D food printers are focusing on the commercial vertical. 3D food printers are more popularly used as chocolate, candy, and bread printing machines as the ingredients required to make these products are easily available. However, the companies such as Nestlé (Switzerland), Barilla (Italy), and Modern Meadow are also working to develop ingredients for other foods, including meat.

Extrusion based printing sub-segment is estimated to account for the

largest market share and the fastest growth in the global 3D food printing

market

Extrusion technology pushes materials into holes at high temperatures and pressures, one layer at a time, and stacks them. Naturally soft materials include puree, jelly, frosting, cheese, and mashed potatoes. Extrusion-based 3Dfood printing is one of the most extensively used and adopted processes among the available options. It is the most affordable 3D printing technology, and because of its low cost, it is also the most popular among small enterprises and households. Thus, their usage is rising rapidly in the 3D food printing sector.

Request for Customization @ https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=267692011

The North American market is estimated to dominate the 3D food printing

market in 2022

The North America is estimated to account for the largest market share in the 3D food printing market in 2022. The presence and growth of the companies offering the 3D food printing technology in this region are boosting the market in this region. This region is projected to be the largest market during the forecast period.

The US is known as one of the early adopters of the new technologies in the world. The busy and fast-moving life of common people makes it hard for them to get the proper nutritious diet. The 3D food printing technology could provide an option to have customized nutritious food. Also, the US government spends the highest amount of budget on healthcare, and the benefits of 3D food printers to provide food rich in specific nutrients and with the ease of chewing and swallowing would provide a suitable option for feeding the aged patients.

This report includes a study of marketing and development strategies, along with the product portfolios of the leading companies in the 3D food printing market. It includes the profiles of leading companies such as 3D systems (US), TNO (Netherlands), NATURAL MACHINES (Spain), Choc edge (UK), Systems & Materials Research Corporation (US), byFlow B.V. (Netherlands), beehex (US), CandyFab (US), ZMORPH S.A (Poland) and Wiiboox (China).