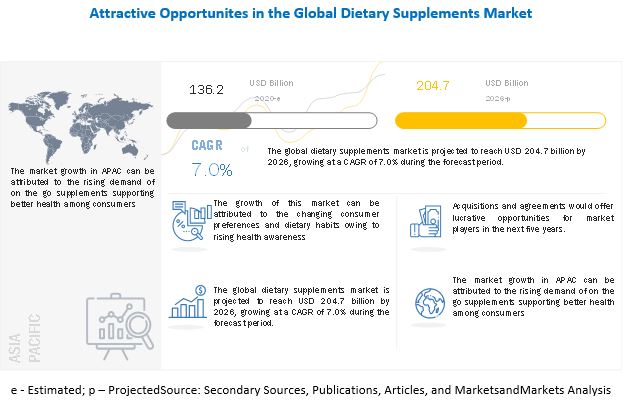

According to MarketsandMarkets, the global dietary supplements market size was valued at USD 136.2 billion in 2020 and projected to reach USD 204.7 billion by 2026, recording a CAGR of 7.0% during the forecast period. The market for dietary supplements is increasingly driven by shifting consumer preferences, rising health awareness, growing geriatric population, and adoption of a healthy diet. The convergence of major industry trends is giving rise to new opportunities for key players in the industry. Changing lifestyles and dietary habits is one of the major factors driving the demand for dietary supplements. The growing positive outlook towards sports nutrition would also positively impact the dietary supplements market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=973

The key players in this market include Amway (US), Herbalife Nutrition (US), ADM (US), Pfizer (US), Abbott Laboratories (US), Arkopharma Laboratories (France), Bayer (Germany), Glanbia (Ireland), Nature’s Sunshine Products (US), FANCL (Japan), Danisco (Denmark), Bionova Lifesciences (India), XanGo (US), Ekomir (Russia), American Health (US), Pure Encapsulations (US), UST Manufacturing (US), Capstone Nutrition (US), Anona GmBH (Germany), Plantafood Medical GmBH (Germany), Carlyle Group (US), Bio-Botanica Inc. (US), GlaxoSmithKline (UK), Nu Skin Enterprises (US), and Nutraceutics (US).

Amway (US) offers effective nutritional & dietary supplements, beauty, and personal care products, and connected home devices. The company operates through four business segments, namely nutrition, beauty, and personal care, and home and others, which include energy drinks and sports nutrition products. It offers dietary supplements under its nutrition segment. Dietary supplements and vitamins are offered under its Nutrilite brand.

The company offers around 450 products in more than 100 countries across regions, such as the Americas, Europe, and Asia Pacific. It operates through 15 manufacturing facilities and processing plants. It has four manufacturing sites in the US, India, China, and Vietnam.

Herbalife Nutrition (US) is a global nutrition company, involved in providing nutrition-based products and solutions for weight management and general wellness. It offers products under various categories, which include weight management, targeted nutrition, energy, sports and fitness, outer nutrition, and literature and promotional products.

It offers dietary supplements under the weight management and targeted nutrition product categories. It operates through four manufacturing facilities, eight quality control laboratories, and a botanical extraction facility across more than 94 countries, including China, Russia, Mexico, the US, and India.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=973

The North American region dominates the dietary supplements market with the largest share in 2020.

North America is projected to hold the largest share in the dietary supplements market. This dominance is driven by the prevalence of chronic diseases due to the hectic lifestyles and increasing awareness among consumers regarding the health benefits of the product. Also, the region has the highest prevalence of obesity. According to the CDC, in the US, the obesity prevalence was 39.8% and affected about 93.3 million adults between 2015 and 2016. Such factors are projected to contribute to the growth of dietary supplements market.